June 20, 2026

Risks of Using AI in Lending (Compliance, Bias & Auditability)

Applications are up. Pipelines are full.

Your underwriters are working longer hours than ever. And yet, loan volumes haven't moved.

If this sounds familiar, you've probably considered hiring. Most lending leaders do. But before you open another requisition, it's worth asking a different question: where is your team's time actually going?

In most institutions, the answer isn't underwriting. It's everything around underwriting: document collection, financial spreading, memo writing, statement reviews, system updates. The capacity problem isn't about people. It's about how much of their day gets consumed by repetitive operational work that has nothing to do with credit judgment.

There's a persistent assumption in lending operations: if throughput is flat, you need more people. But adding underwriters doesn't automatically increase the number of loans your team can process. Why? Because every new hire inherits the same workflow bottlenecks as everyone else.

A senior underwriter might spend only 30–40% of their day on actual credit analysis. The rest goes to gathering documents, validating data, reformatting spreadsheets, and drafting narratives that repeat information already sitting in three different systems.

Capacity isn't headcount. It's the time available for judgment.

When you reframe the problem this way, the solution shifts. Instead of asking who else can we hire?, the better question becomes what work can we remove from the people we already have?

Most capacity doesn't vanish in one dramatic bottleneck. It leaks steadily across the workflow—an hour here chasing a tax return, forty minutes there rebuilding a spread. These are the five areas where lending teams lose the most time.

Before any credit analysis begins, someone has to collect tax returns, financial statements, personal guarantees, entity documents, and IDs. When items are missing, and they usually are, the back-and-forth with borrowers can stretch for days.

Underwriters end up functioning as document coordinators instead of credit analysts. Every hour spent chasing a missing Schedule K-1 is an hour not spent evaluating risk.

Once documents arrive, the spreading begins. Teams manually key figures from tax returns and financial statements into spreadsheets or origination systems. It's copy-paste work that demands concentration but adds no analytical value.

A single commercial loan might require spreading three years of business returns, personal financial statements, and interim financials, easily two to three hours of manual data entry per deal, with multiple reviews to catch errors.

Analyzing bank statements is tedious and time-intensive. Teams categorize transactions, calculate average balances, assess cash flow patterns, and evaluate liquidity, often across multiple accounts and multiple months.

For small business and commercial loans, this step alone can take an underwriter a significant portion of their day on a single file.

The credit memo is where analysis becomes narrative. But in practice, much of what goes into a memo is restatement—summarizing financial data, describing the borrower, and restating terms. Underwriters spend hours writing documents that largely organize information already available in the file.

When memos run late, committee meetings slip. When committees slip, approvals delay. The downstream impact of slow memo preparation is larger than most teams realize.

Capacity drains don't stop at origination. Relationship managers and credit teams spend significant time collecting updated financials, tracking covenant compliance, and preparing for annual reviews. In many institutions, portfolio monitoring happens quarterly at best—not because it isn't important, but because there simply isn't enough bandwidth to do it more frequently.

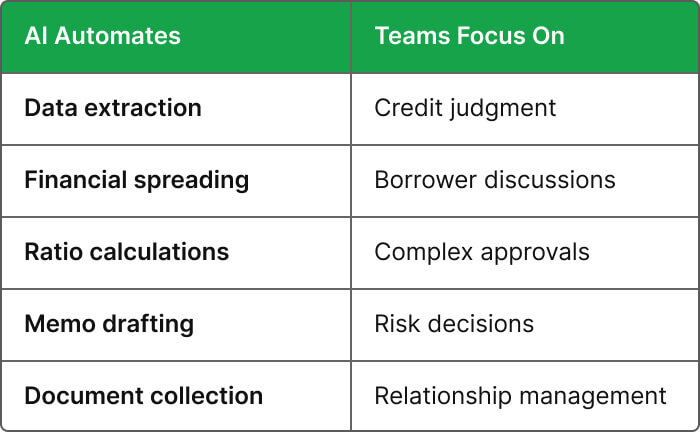

The teams that have solved this problem didn't do it by working faster. They did it by removing operational work from the underwriting process entirely. Here's what that looks like across the workflow:

A reasonable concern with any automation is whether it introduces new risk. In practice, the opposite tends to be true. When you separate what AI handles from what your team focuses on, the division is clear:

The work being automated is administrative. The work staying with your people is analytical. That's not a risk tradeoff, it's a better allocation of expertise.

Not every team recognizes the problem immediately. These are the signals worth watching:

If three or more of these sound familiar, the constraint isn't your team's effort. It's their workflow.

When you recover even a few hours per underwriter per day, the compounding effects are significant:

These aren't aspirational metrics. They're the direct result of reallocating time from administrative tasks to the work that actually requires human judgment.

Most lending teams don't have a technology problem, they have a capacity problem. Every loan moves through document collection, financial analysis, cash flow review, credit memo preparation, and ongoing portfolio monitoring. Each step requires manual effort, repeated data entry, and constant coordination between teams.

Uptiq automates these operational tasks with specialized AI agents built for each stage of the lending lifecycle. Instead of relying on a single model to handle everything, dedicated agents perform the work they are designed for:

Each agent works within your existing systems and credit policies, allowing underwriters and credit teams to focus on judgment instead of repetitive administrative work.

Most institutions assume growing loan volumes require hiring more underwriters. In reality, much of an underwriter's day is spent collecting information, re-keying data, preparing documentation, and following up on missing items rather than evaluating credit risk.

When those manual activities are automated, the same team can process significantly more loans without compromising quality or consistency. Decisions move faster, operational bottlenecks shrink, and experienced underwriters spend their time where they create the most value.

The institutions gaining an advantage aren't simply adding headcount to keep up with demand. They're building lending operations that scale through better execution: recovering hours on every loan and turning existing teams into higher-capacity, higher-impact organizations.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.