June 18, 2026

AI vs Rule-Based Systems in Credit Decisioning: What's the Difference?

AI adoption in lending is accelerating, and so is the hesitation surrounding it. For most financial institutions, the technology itself is not the obstacle. Trust is.

Chief Risk Officers want to know whether AI decisions can be explained under examination. Chief Compliance Officers want to understand how bias is detected and controlled. Heads of Credit want assurance that policy is being applied consistently, not approximated. These are not objections to AI. They are the right questions, and they are going unanswered by most of the AI products currently being marketed to financial institutions.

The good news is that the concerns are legitimate precisely because they are solvable. The risks associated with AI in lending are real, but they are governance risks, not technology risks. They arise not from AI being inherently unreliable, but from AI being deployed without the policy controls, explainability standards, and human oversight mechanisms that regulated lending requires.

The biggest risk isn't using AI in lending. It's deploying AI without governance, explainability, policy controls, and human oversight.

Most conversations about AI in lending focus on capability, what the model can do, how accurate its outputs are, which use cases it handles well. These are relevant questions. They are not the questions that determine whether an AI deployment succeeds in a regulated financial institution.

What lending executives actually need from AI is not a more capable model. It is a deployment that can answer the questions a regulator will ask: How was this output produced? What data was it based on? Who reviewed it? What would happen if we ran it again? Can you show us the audit trail?

A highly capable AI model that cannot answer these questions will not survive the first examination cycle. A more modest AI system built on a governance-first architecture — with policy-aware workflows, source-level traceability, human oversight at every decision point, and immutable audit logs will. Governance is not a constraint on AI deployment in lending. It is the foundation that makes production deployment possible.

THE RISK: Financial institutions operate under fair lending requirements, consumer protection regulations, internal credit policies, and ongoing regulatory examination. AI that cannot demonstrate how its outputs were produced, which inputs, which logic, which version of the model — creates compliance exposure that no institution can accept. An examiner who cannot get a clear answer about how a lending decision was made does not give partial credit for effort.

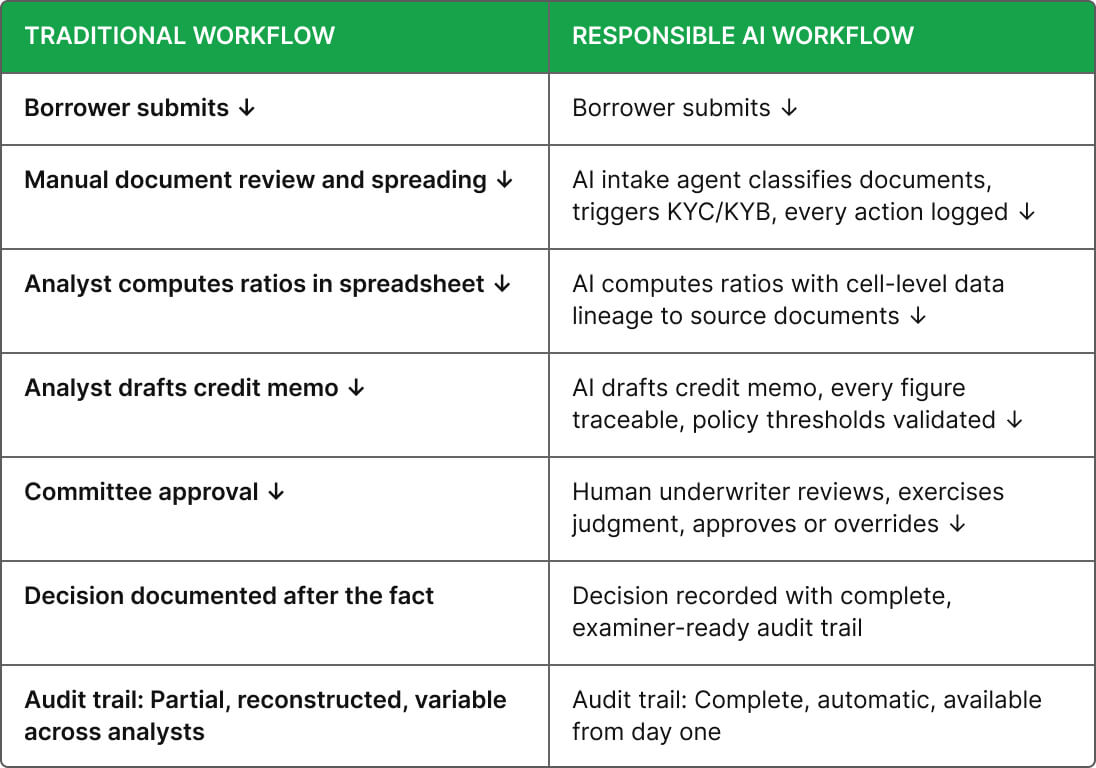

GOVERNANCE APPROACH: Every AI workflow should be configured to the institution's specific credit policies, not a vendor's generic defaults. Outputs must be explainable in human terms at every level of detail. Human approval should be structurally required before any AI-assisted output influences a credit decision. The audit trail should be produced automatically as a byproduct of normal operation, not assembled after the fact for examination purposes.

OUTCOME: Compliance teams can trace every AI-assisted output to its source, confirm that policy was applied consistently, and demonstrate to examiners that human judgment remained accountable for every consequential decision.

THE RISK: Bias in lending is not a new risk introduced by AI, manual underwriting processes have long produced inconsistent outcomes when individual analysts apply policy differently, weight qualitative factors subjectively, or make judgments influenced by information that should not affect a credit decision. AI can inherit these patterns from training data, amplify them at scale, and make them harder to detect because the inconsistency is embedded in the model rather than visible in individual analyst behavior.

GOVERNANCE APPROACH: The governance response to bias risk is standardization, not removal. AI agents that apply consistent financial analysis, using the same definitions, the same analytical framework, and the same policy thresholds on every application, produce more consistent outcomes than analyst-to-analyst manual review. Human oversight provides the check on cases where contextual judgment is needed. Continuous monitoring of output patterns surfaces any systematic deviation before it accumulates into a material fair lending exposure.

OUTCOME: Credit decisions become more consistent across borrower populations, more defensible under fair lending examination, and more aligned with stated policy than manual processes at scale typically achieve.

THE RISK: Examiners expect institutions to answer specific questions about every lending decision: why was this application approved, where did this ratio come from, who reviewed this output, how was this conclusion generated. Generic AI tools that produce probabilistic outputs without source attribution cannot meet this standard. An output that cannot be traced to its inputs is not usable in a regulated lending workflow regardless of how accurate it is on average.

GOVERNANCE APPROACH: Finance-native AI agents produce outputs with cell-level data lineage, every calculated ratio traceable to the specific line item, document, and page that produced it. Every workflow step is logged with a timestamp and a record of what the agent did, what the human reviewer did, and what the final output was. This audit trail is produced continuously as a byproduct of normal operation and is available for examination without requiring any post-hoc reconstruction.

OUTCOME: The audit trail produced by a well-governed AI deployment is more complete and more consistent than the documentation produced by manual processes — and it satisfies examiner expectations without requiring additional compliance effort.

THE RISK: General-purpose AI models can generate plausible-sounding outputs that are not grounded in the actual data provided, inventing financial figures, summarizing documents inaccurately, or producing conclusions that cannot be traced to a verifiable source. In a consumer or productivity application, this is an inconvenience. In a lending workflow, where outputs influence decisions that affect borrowers and carry regulatory accountability, it is a material risk.

GOVERNANCE APPROACH: Financial AI systems designed for lending workflows constrain outputs to information traceable to verified source documents. The agent does not infer or extrapolate it extracts, categorizes, and computes from the actual documents in the file. Every output is grounded. Every figure has a source. Human review at each stage provides the validation layer that catches any output that does not meet the institution's standards before it influences a decision.

OUTCOME: Lending teams can rely on AI outputs with the same confidence they would place in analyst work because the outputs are held to the same standard of traceability and are reviewed by qualified professionals before they influence any decision.

THE RISK: The most significant governance failure in AI deployments is not a technology problem, it is a design problem. Systems that allow AI to influence consequential decisions without a structurally required human review step create accountability gaps that neither institutions nor regulators can accept. The concern is not that AI will make bad decisions. It is that bad decisions will be made without anyone being clearly accountable for reviewing them.

GOVERNANCE APPROACH: Human oversight should not be optional in AI lending workflows, it should be structural. The design principle is explicit: AI extracts, calculates, summarizes, and monitors. Humans review, interpret, and approve. Exception routing ensures that cases outside standard parameters reach a qualified reviewer before any decision is made. Override capability is available at every step, and every override is logged. The human remains accountable for every consequential output.

OUTCOME: Lending institutions can deploy AI at scale without accepting governance gaps. The team retains full accountability for every decision. AI eliminates the operational work surrounding decisions without removing the professional judgment that defines them.

Across the five risks above, a consistent set of governance requirements emerges. Use this as a self-assessment framework before selecting an AI deployment for any lending workflow:

✓ Human-in-the-loop review is structurally required at every decision point, not optionally available

✓ Workflows are configured to the institution's specific credit policies, not a generic model's defaults

✓ Every output is explainable in human terms and traceable to its source data

✓ Cell-level data lineage is available for every calculated figure, document, page, and line item

✓ Immutable audit logs capture every agent action, human review, and override decision

✓ Exception routing directs out-of-policy cases to qualified reviewers automatically

✓ Governance controls are embedded in the deployment architecture, not layered on afterward

✓ The system integrates with existing LOS and core infrastructure, no replacement required

The governance standard: Any AI output that cannot be traced, explained, reviewed, and overridden is not appropriate for use in a regulated lending workflow. This is not a high bar. It is the minimum.

What this demonstrates: AI accelerates the work without removing accountability. The human remains responsible for every decision. The audit trail is stronger than the manual process it replaces.

Uptiq's AI agents are built on a governance-first architecture, every design decision reflects the accountability requirements of regulated financial institutions, not the capabilities of a general-purpose AI model.

Policy awareness: Every agent is configured to the institution's specific credit policies, approval thresholds, and document templates. The AI operates within the institution's rules, it does not apply a vendor's generic defaults.

Explainability: Every output is linked to its source data with cell-level traceability. A computed DSCR is traceable to the specific line item, document, and page that produced it. No black-box outputs.

Human oversight: Exception routing directs out-of-policy cases to qualified reviewers automatically. Override capability is available at every step. Every override is logged. Human approval is structurally required before any output influences a decision.

Auditability: Immutable audit logs capture every agent action, every human review, every override, and every workflow decision, produced automatically as a byproduct of normal operation, available for examination without additional documentation effort.

Integration: Agents connect to existing LOS, core banking systems, and CRM infrastructure. No infrastructure replacement. The governance framework works within the systems the institution already operates.

The institutions that are successfully deploying AI in lending are not the ones that have found ways to work around compliance, bias, and auditability concerns. They are the ones that built those requirements into the deployment architecture from the beginning, and discovered that doing so made the technology more valuable, not less.

When AI outputs are explainable, examiners gain confidence rather than raising objections. When workflows are policy-aligned, credit decisions become more consistent, not less controlled. When human oversight is structural, accountability is clearer than it ever was in manual processes. Governance, implemented correctly, is not a constraint on AI in lending, it is what makes production AI trustworthy enough to scale.

The future of lending won't be built on AI alone. It will be built on AI that institutions can explain, govern, audit, and trust. The organizations that succeed won't be the ones deploying the most AI, they'll be the ones deploying AI responsibly.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.