July 2, 2026

Why Workflow Automation Tools Fail in Lending

Lending

Automation delivered on its promise, at least the first part of it.

Lending teams moved fast. Paper trails became digital records. Disconnected email threads became structured workflows. Manual intake processes moved online. For a while, it felt like the hard work was done.

And in fairness, it solved something real. Analysts spent less time chasing documents and more time doing the work they were actually hired to do. Operations teams finally had systems they could rely on.

But the finish line turned out to be further away than anyone expected.

Despite better tools, teams still face:

Though automation improved how work flows, it didn't change how analytical work gets done. Humans still interpret financials, validate collateral, draft credit memos, and structure complex deals.

This is where the conversation is shifting - from automation to delegation.

Traditional automation is genuinely good at what it does. Routing applications to the right teams. Sending notifications for missing documents. Triggering approval workflows based on predefined thresholds. Moving files between compliance, credit, and operations systems.

But lending operations involve a lot more than that. The work that actually drives decisions requires analysis, context, and judgment:

Interpreting trends across months of bank statements and tax returns. Validating equipment schedules against invoices and UCC filings. Assessing borrower cash flow patterns and real debt capacity. Drafting credit memos that synthesize financial health and collateral value. Structuring financing offers that balance risk against policy constraints.

These aren't tasks you can reduce to a set of rules. And that's exactly where rules-based automation plateaus.

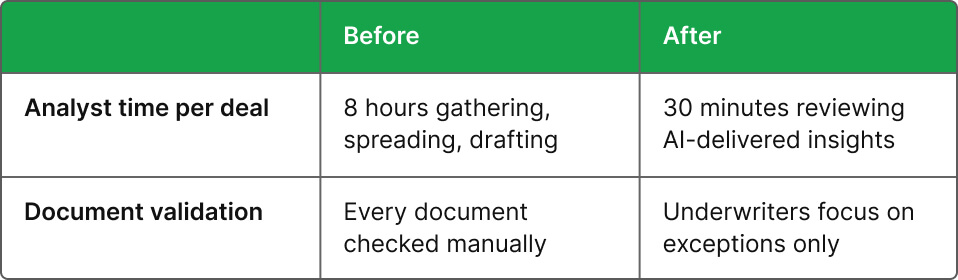

The result? Even sophisticated lenders report underwriting teams spending 60% of their time on document review rather than actual risk analysis. Analysts manually compile financial spreads from disparate sources. Credit memos consume eight to twelve hours per deal despite having automated workflows in place. Decision cycles average 25 to 40 days, even with digital intake.

Automation perfected the pipes. But the analytical workload stayed stubbornly human.

AI delegation isn't some polished version of automation. It's a fundamentally different concept.

Automation executes predefined steps. Delegation performs parts of the work itself. Instead of routing an equipment lease application to an analyst, AI systems now:

AI essentially moves from workflow facilitator to analytical collaborator.

What that looks like in practice:

AI delegation doesn't replace lending expertise. It eliminates the repetitive analytical grind. AI agents designed by Uptiq help equipment finance lenders achieve this- Underwriting capacity gets doubled without headcount growth across 150+ operations, cutting cycles 41% faster.

Traditional lending workflows follow a predictable but heavily manual pattern. Application intake leads to manual document collection. Document review means analysts validating uploads one by one. Financial analysis involves manually spreading P&Ls and balance sheets. Credit memo drafting requires analysts to synthesize everything they've found. Risk evaluation is a judgment call made by the underwriter. Deal structuring means creating term sheets by hand. Contract preparation involves legal teams rekeying approved terms from scratch.

AI-delegated workflows fundamentally change this sequence. At every stage.

Uptiq delivers this redesign to equipment lessors, collapsing weeks of packaging into days while scaling 2x volume with the same front office.

The redesigned model collapses weeks of packaging into days. Human effort shifts from data aggregation, which was consuming 70% of analyst time, to decision validation. Operations scale twice as fast without front-office hires.

The impact is measurable, and it's showing up across the industry.

For equipment finance specifically, AI delegation addresses the pain points that matter most:

Uptiq equipment finance customers report maintaining front-office staffing while doubling deal flow, proving operational capacity is no longer the constraint.

The shift moves from operational capacity limits to strategic risk appetite. Lenders who master delegation don't just move faster, they build credit operations that compound efficiency as volumes keep growing, turning ops into a competitive moat.

It's worth being clear about something one thing: AI delegation amplifies lending expertise. It doesn't replace it.

Final credit decisions stay with people because they need to. They require institutional risk tolerance, portfolio strategy, an understanding of market conditions, long-term borrower relationships, and judgment around complex collateral scenarios like specialty equipment and cross-collateralization. None of that is something AI can fully own.

What changes is how analysts and underwriters spend their time.

Analysts shift into a validation role, hence, checking AI insights against their own experience, handling exceptions and edge cases, applying qualitative judgment to quantitative signals, and structuring creative solutions within policy bounds. Underwriters become strategic risk managers. They are now more focused on portfolio-level risk allocation, evaluating deal structures that require a human perspective, and championing exceptions that need senior oversight.

AI handles around 80% of the repetitive analytical workload. Humans own the 20% that requires wisdom, context, and real accountability. That's not deskilling lending professionals. In reality, it is elevating them to the work that actually matters most.

Automation digitized lending processes, while AI delegation reimagines them entirely.

As equipment finance volumes surge and documentation complexity keeps growing, manual-analysis models will crack under the pressure. The lenders who come out ahead will be the ones who combine automated workflows for routine tasks, AI delegation for analytical heavy lifting, and human judgment for strategic decisions.

The result isn't just speed, though speed matters. It's operational resilience that scales with market demand while keeping credit discipline fully intact.

Lenders who adapt to delegation gain more than efficiency gains on a dashboard. They build competitive moats through superior execution, the kind that's hard to replicate and compounds over time.

Operational agility is becoming the ultimate risk management tool. The future belongs to teams that learn to delegate effectively, well before their competition does.

Ready to see what AI delegation looks like inside your credit workflows? Book a demo with Uptiq and find out how much capacity your team is leaving on the table.

Automation focuses on executing predefined rules and workflows. For example, routing applications, triggering notifications, or moving documents through systems.

AI delegation goes a step further by performing parts of the analytical work involved in lending operations. AI systems can extract information from financial documents, analyze bank statements, identify credit signals, and draft structured summaries such as credit memos.

In other words, automation manages the process, while AI delegation contributes to the work itself.

AI can assist with several operational tasks that traditionally required significant manual effort. These include:

These capabilities help analysts and underwriters focus more on decision-making rather than time-consuming data preparation.

No. AI delegation is designed to support lending teams rather than replace them.

Credit decisions often depend on factors such as borrower relationships, industry dynamics, risk tolerance, and portfolio strategy. These are areas where human judgment remains essential.

AI systems help by preparing data, surfacing insights, and drafting analysis so that underwriters and analysts can focus on evaluating risk and making informed decisions.

One of the biggest constraints in lending operations is the amount of time analysts and underwriters spend reviewing documents and compiling financial analysis.

By automating parts of this analytical work, AI allows teams to process more applications without proportionally increasing headcount. This helps lenders increase deal throughput, reduce underwriting bottlenecks, and maintain operational efficiency as application volumes grow.

Successful adoption requires more than just implementing new technology. Lenders should evaluate:

When implemented thoughtfully, AI can complement existing processes while improving speed, consistency, and scalability across lending operations.