The most persistent misconception about AI in underwriting is about what it is changing. Most of the conversation focuses on whether AI will replace underwriters — on automated credit decisions, algorithmic approvals, and machines making calls that humans used to make.

That is largely the wrong conversation. The actual change AI is driving in underwriting is not at the decision stage. It is at every stage before it.

Ask an underwriter to account for their day honestly. Credit judgment, the analysis of risk, the evaluation of a borrower's capacity and character, the final call, is often a small fraction of total elapsed time. The rest goes to document collection, financial spreading, bank statement review, credit memo writing, ratio validation, and system updates. These tasks are necessary. They are also largely mechanical. And they are consuming the capacity of the most experienced, most expensive people in the credit operation.

AI is changing underwriting by targeting that mechanical layer, automating the work that surrounds the credit decision so that the people making decisions can spend their time doing exactly that.

AI handles documents, calculations, and summaries. Underwriters handle decisions. That division is the entire shift.

What AI Actually Does in Underwriting

AI in underwriting does not approve or decline loans. It automates the operational tasks that currently consume analyst capacity before the credit judgment can begin.

In practice, that means: classifying and extracting data from incoming loan documents, spreading multi-year financial statements into structured templates, categorizing bank transactions and computing cash flow metrics, drafting the credit memo narrative, validating computed ratios against policy thresholds, and surfacing exceptions for underwriter review. Every one of these tasks currently requires human time. None of them requires human credit judgment.

The core design principle: AI handles what is structured, repetitive, and rules-based. Underwriters handle what requires professional judgment, relationship context, and institutional accountability. Human oversight applies at every stage.

Where Underwriters Actually Spend Their Time

Document collection: Borrower files arrive incomplete, missing schedules, unsigned forms, and wrong fiscal year. Operations teams spend days chasing gaps before the underwrite can open.

Financial spreading: Extracting line items from tax returns and CPA statements, entering them into a template, building out DSCR and leverage ratios manually, two to four hours per deal, longer on multi-entity structures.

Bank statement review: Scrolling through months of transaction history to identify overdraft patterns, undisclosed debt obligations, and cash flow behavior. High effort, high fatigue, inconsistent output across volume.

Credit memo preparation: Translating a completed analysis into a formatted narrative, structuring the policy rationale, embedding the ratios, and aligning the output with the committee template. One to two hours after the analysis is already done.

Policy validation: Manually checking computed ratios against policy thresholds, flagging exceptions, and routing them through an escalation process with no automated tracking.

The pattern across all five is the same: skilled professionals doing structured, repetitive work that no longer needs to sit on their desk.

Five Real Workflow Examples

The following examples show how each manual bottleneck changes when AI handles that specific workflow, not in theory, but in the operational sequence that lending teams actually follow.

WORKFLOW 1 AI-Powered Intake

BEFORE: Operations teams manually sort PDFs, emails, and uploaded files. Documents are classified by hand, completeness is assessed by eye, and missing items are chased through email follow-ups. Days pass before the underwriter receives a complete file.

AFTER: An intake agent classifies every incoming document automatically, assesses completeness against a configurable checklist, triggers KYC and KYB verification in parallel, and initiates follow-up requests for missing items — all from the moment the application is submitted.

OUTCOME: Underwriters open a complete, structured loan file rather than a queue of documents to organize. Document collection time drops from days to hours.

WORKFLOW 2 Automated Financial Analysis

BEFORE: Analysts manually extract line items from tax returns and CPA-prepared statements, enter them into spreading templates, and build DSCR, leverage, and liquidity ratio calculations by hand. Formula errors compound across multiple documents and fiscal periods.

AFTER: A financial analysis agent extracts data directly from financial statements, normalizing across formats, applying consistent policy-aligned definitions, and computing all key ratios automatically with full data lineage traceable to the source document.

OUTCOME: Financial spreading moves from two to four hours of manual work to minutes of automated computation. Outputs are consistent across every deal, regardless of which analyst reviews them.

WORKFLOW 3 Bank Statement Analysis

BEFORE: Teams scroll through hundreds or thousands of transactions per borrower, manually categorizing each entry, identifying recurring obligations, and computing cash flow averages. Accuracy degrades with volume as analysts fatigue from large packages.

AFTER: An AI agent processes every transaction automatically, categorizing operating expenses, debt service, and transfers; flagging NSF clusters and undisclosed obligations; computing average monthly cash flow and burn rate — and delivers a structured behavioral summary.

OUTCOME: Analysts evaluate risk signals rather than excavate them. Detection is more complete and more consistent than manual review at high volume.

WORKFLOW 4 Credit Memo Generation

BEFORE: Underwriters spend one to two hours after completing the analysis translating their work into a formatted credit memo — writing the narrative, embedding the ratios, structuring the policy rationale, and matching the committee template. Memos routinely delay committee meetings.

AFTER: A credit memo agent drafts the narrative automatically once the analysis is complete — structuring the policy rationale, embedding computed ratios, and formatting the output to match the institution's template. The underwriter reviews, edits where judgment requires, and approves.

OUTCOME: Credit memo preparation time drops from hours to minutes. Committee scheduling is no longer held up by documentation lag.

WORKFLOW 5 Continuous Portfolio Monitoring

BEFORE: Relationship managers and credit teams conduct quarterly reviews by manually collecting updated borrower financials, re-spreading statements in spreadsheets, and checking covenant ratios against thresholds. Risk signals surface weeks after they become relevant.

AFTER: A monitoring agent re-spreads borrower financials on a defined schedule, calculates updated covenant ratios, scores breach likelihood continuously, and surfaces exceptions to the relationship manager when they occur, not at the next scheduled review.

OUTCOME: Portfolio risk management shifts from periodic review to continuous oversight. Teams identify issues earlier and spend less time on manual collection cycles.

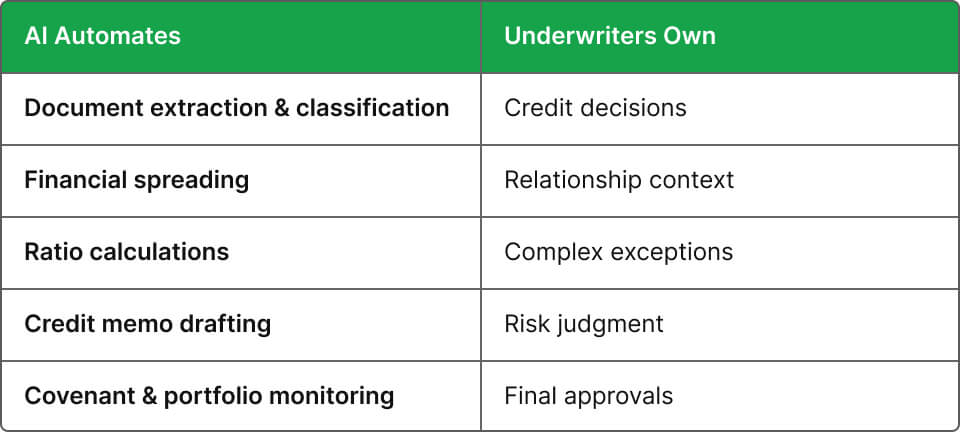

What AI Should Automate, And What Underwriters Should Own

The distinction that matters most in any discussion of AI underwriting is not capability — it is responsibility. The following division reflects how well-designed AI deployments actually work:

Human oversight is not optional in this model. It is structural. Every AI output is reviewable, traceable to its source, and overridable by the underwriter. The credit decision remains with the professional. What changes is the quality and completeness of the analysis on which the decision is based.

The Benefits Beyond Speed

More applications per underwriter: removing the administrative layer from each workflow stage allows the same team to process significantly more volume of institutions using AI agents across the underwriting workflow, report 2× application throughput without growing the team.

Consistent credit analysis: when spreading, ratio calculation, and policy validation follow the same logic on every deal, the analyst-to-analyst variation that produces policy drift at scale is eliminated. Every borrower file is analyzed the same way.

Reduced manual errors: formula errors in manual spreads, missed transactions in statement review, and version discrepancies in document handling disappear when the computation is automated, and the output is traceable.

Better audit readiness: AI outputs carry full data lineage from the source document to the computed ratio. Examiner reviews are straightforward rather than requiring the team to reconstruct how a calculation was performed.

Lower operational costs: The cost per loan decreases as analyst hours focus on judgment rather than assembly. Operational cost reductions of 29% or more are typical when the administrative layer is automated.

How Banks and Lenders Adopt AI Incrementally

The institutions that see the most consistent results from AI underwriting do not implement everything at once. They start with the highest-friction bottleneck, demonstrate measurable impact, and expand from a foundation of operational confidence.

A practical adoption sequence:

Phase 1 - Intake: highest immediate impact on cycle time, fastest demonstration of value. Document collection and KYC/KYB orchestration automated first.

Phase 2 - Financial spreading: the largest single time drain removed from the analyst's workload. Consistent, policy-aligned outputs from day one.

Phase 3 - Bank statement analysis: deeper risk intelligence without additional analyst hours. Detection improves as volume scales.

Phase 4 - Credit memo generation: the final pre-decision bottleneck removed. Committee scheduling no longer constrained by documentation lag.

Phase 5 - Continuous monitoring: post-close portfolio oversight automated. Risk signals surface before they become problems rather than after.

Each phase builds on the previous one. The governance framework and integration work from phase one support every subsequent deployment without being rebuilt from scratch.

How Uptiq Supports Modern Underwriting

Uptiq deploys finance-native AI agents across each stage of the underwriting workflow, each one purpose-built for a specific task, each one integrated with the LOS, core banking systems, and CRM infrastructure the institution already uses. No replacement of existing systems. The agents layer over what is already in place and add the execution layer that coordinates it.

The Intake Superagent handles document classification, completeness assessment, and KYC/KYB orchestration. The Underwriting Superagent manages financial spreading, bank statement analysis, ratio computation, and credit memo generation. The Continuous Monitoring Superagent handles post-close portfolio oversight: re-spreading financials on schedule, scoring covenant breach likelihood, and surfacing exceptions proactively.

Every agent operates within the institution's existing credit policy. Every output is explainable, source-traced, and audit-ready. The underwriter retains full control of every credit decision. What changes is how much of the day remains for making them.

On integration: Uptiq connects to existing LOS, CRM, and core banking systems — no rip-and-replace. Most institutions are live on the first workflow within weeks, not months.

What Is Actually Changing

AI is not changing underwriting by making credit decisions faster or by replacing the judgment that defines a sound lending operation. It is changing underwriting by removing the operational work that currently prevents underwriters from exercising that judgment at the pace and scale the market requires.

The lenders gaining ground are not doing it by automating credit decisions. They are doing it by automating document intake, financial spreading, cash flow analysis, memo generation, and portfolio monitoring, and concentrating their team's expertise on the work that actually requires it.

AI isn't changing underwriting by replacing expertise. It's changing underwriting by eliminating repetitive work, giving lending teams more time for judgment, consistency, and borrower relationships.

About the Author

Armi (Armine) Movsesyan-Susanyan

Vice President - Digital Banking

Armi Movsesyan-Susanyan is Vice President of FI Success at UPTIQ, with over 8 years of experience in sales and account management across fintech and financial services. She is passionate about empowering community financial institutions with actionable data and tools that help small businesses grow.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.