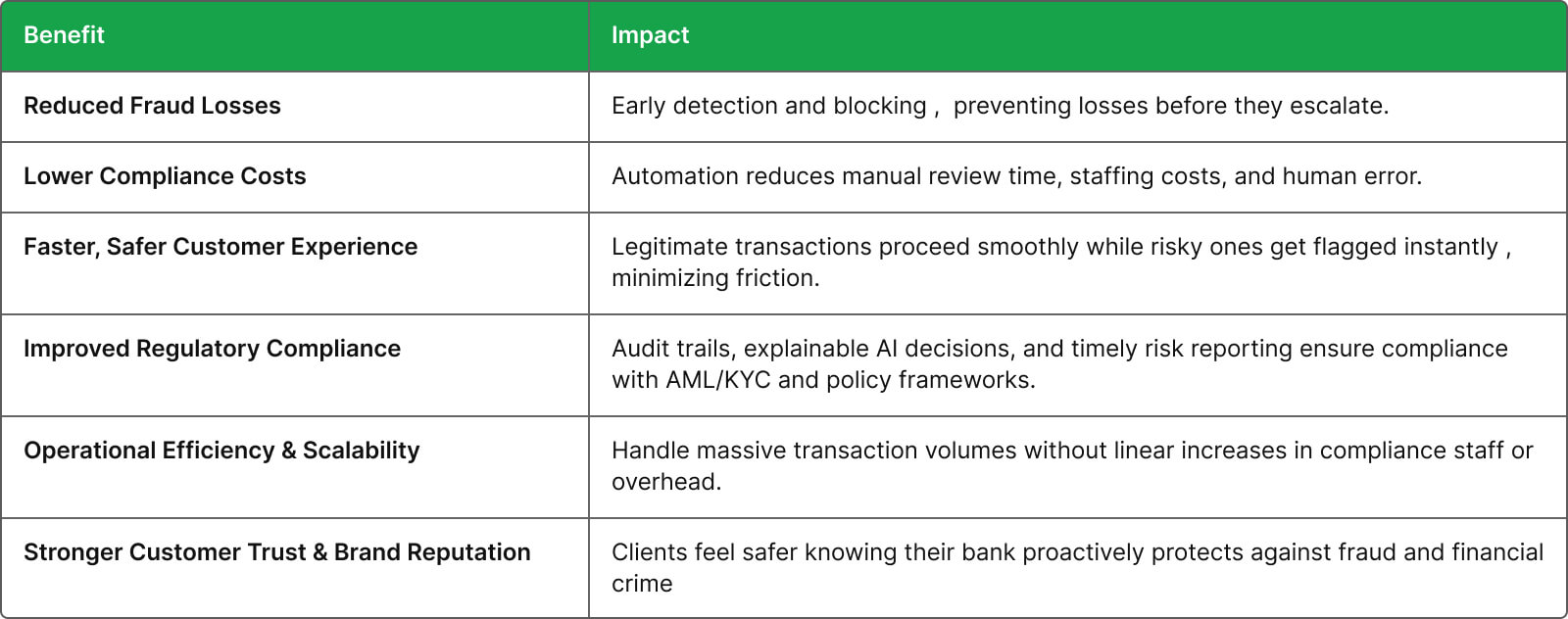

Fraud, money laundering, and financial crime are escalating at an alarming rate, driven by digital banking, instant payments, global connectivity, and increasingly sophisticated criminal tactics. For banks, fintechs, and credit unions, the cost of inaction is steep: financial loss, regulatory penalties, reputational damage, and , most importantly , loss of customer trust.

Recent data shows many banks, credit unions, and fintechs face thousands of fraud attempts per year, with a significant portion resulting in major losses.

Traditional rule-based and manual review systems simply can’t keep pace with the speed, volume, and complexity of modern transactions.

That’s why in 2026, AI-driven real-time fraud and AML detection isn’t optional , it’s essential.

With the right AI infrastructure, financial institutions can move from reactive defense to proactive prevention: stopping threats before they inflict harm, while improving compliance efficiency and operational resilience.

Why Traditional Methods Are No Longer Enough

Banks historically relied on batch-mode reviews, periodic audits, and static “if-then” rules to flag suspicious activity. While these methods once sufficed, they now fall short:

Scale & speed mismatch: With thousands of transactions per minute, manual or rule-based systems can’t monitor every activity in real time.

Static rules = limited detection: Fraudsters constantly adapt , using synthetic identities, mule-accounts, atypical transfer patterns. Static rules struggle to catch novel fraud types.

Volume of false positives, overwhelming compliance teams and slowing down operations.

Regulatory complexity: AML rules, KYC requirements, cross-border payments , manual compliance is error-prone and inefficient.

Given rising fraud losses , with many institutions reporting 500 k USD+ direct losses in a year, the need for smarter, real-time defenses is clear.

How AI Changes the Game: Real-Time, Adaptive, Intelligent Detection

AI systems , especially those leveraging machine learning (ML) and behavioral analytics , can inspect every transaction as it happens. They compare patterns against historical data, peer-group benchmarks, and known risk signals. Unlike rule-based systems, AI can:

Detect subtle anomalies: e.g. sudden changes in volume, geography, timing, or account behavior.

Flag complex fraud patterns: mule networks, laundering attempts, synthetic identities, or deep-fake aided scheme.

Adapt over time: as fraud tactics evolve, the AI learns and updates its detection logic.

This capability transforms fraud prevention from reactive investigations to proactive blocking.

2. Smarter AML & Compliance Monitoring

Compliance teams bear the brunt of regulatory pressure , KYC, AML, sanction screening, suspicious activity reporting. AI helps by:

Automatically scanning transactions, customer profiles, behavioral patterns for money-laundering indicators.

Flagging suspicious accounts or transactions in real time, enabling faster investigation.

Reducing manual workload and human error, ensuring compliance at scale without sacrificing speed.

With recent regulatory fines and increasing AML expectations, AI-driven compliance enables institutions to stay ahead.

3. Continuous Learning & Adaptive Defense

Unlike static systems, AI-based fraud/AML engines evolve. As new fraud patterns surface , like synthetic identity fraud, Generative-AI–driven scams, account takeovers , AI models retrain to recognize them, enhancing detection over time.

This continuous learning ensures long-term resilience: financial crime evolves, and AI evolves with it.

How Uptiq’s AI-Driven Platform Enables Modern Real-Time Fraud & AML Detection

At Qore and Uptiq’s broader AI banking stack, we build systems that help financial institutions fight fraud and financial crime , while staying nimble, compliant, and customer friendly.

Real-time Data Processing & Scalability

Process millions of transactions per minute across channels , digital banking, payments, wire transfers , in real time.

Unified data infrastructure ensures consistent visibility and context across accounts, devices, geographies, and channels.

AI-First Fraud & AML Engine

Machine learning models analyze behavior, transaction patterns, device metadata, and external threat intelligence to detect fraud or money-laundering signals.

Maintains record-keeping, logs, and compliance documentation , offering defensibility during audits or investigations.

Why 2026 Is the Make-or-Break Year for AI in Fraud & AML

As financial crime evolves , with deepfakes, Gen-AI scams, mule networks, synthetic identities , the complexity of detection far outpaces human capability. Research suggests that by 2026, most leading banks and fintechs will rely heavily on AI-based detection systems to stay secure.

For institutions delaying adoption, risks of loss or regulatory penalty grow. For those that act now, AI-driven fraud and AML detection becomes not just a compliance need , but a competitive differentiator.

Implementation Considerations & Best Practices

When deploying AI-driven fraud and AML systems, institutions should:

Use High-Quality, Clean Data: AI is only as good as the data it analyzes , ensure consistent, accurate transaction logs, customer metadata, device info.

Combine AI With Human Oversight: For sensitive or high-risk alerts, maintain human-in-the-loop review for nuanced judgment.

Design for Explainability & Compliance: Maintain audit trails, transparency in decision logic , critical for regulators and internal governance.

Continuously Retrain & Update Models: Fraud evolves , retrain models regularly with new data and emerging threat patterns.

Balance Security with Customer Experience: Avoid excessive false positives; calibrate sensitivity thresholds to minimize friction for legitimate customers.

Plan for Scalable Infrastructure: Ensure systems handle high transaction volumes without performance degradation , something Uptiq’s platform is designed to support.

AI Isn’t Optional , It’s Essential

In 2026, real-time fraud and AML detection powered by AI will be the baseline , not the exception. Institutions that invest in AI-driven fraud prevention now will not only reduce losses, but gain customer trust, scalable compliance, operational efficiency, and a competitive edge.

With Uptiq’s AI-enabled banking infrastructure, financial institutions , from banks to credit unions and fintechs , can transform fraud defense from a reactive burden into a proactive, intelligent shield.

Ready to see how Uptiq’s AI Agents can safeguard your institution against fraud & money-laundering?