July 2, 2026

Why Workflow Automation Tools Fail in Lending

Most financial institutions have experimented with large language model workflows by now. A chatbot answering employee questions. A document summarizer reducing reading time. A prompt-based interface that generates draft reports or emails. The outputs are impressive. The pilots are easy to demonstrate.

And then someone asks the harder question: what did it actually change in the operation?

This is where the distinction between LLM workflows and AI agents becomes important, not as a technical nuance, but as a practical question about what kind of AI a financial institution actually needs to generate measurable operational value. Generating a well-written summary of a financial statement is not the same as spreading that statement, computing the ratios, validating them against credit policy, and routing the output to the underwriter with a complete audit trail. One produces content. The other executes work.

The institutions moving from AI experimentation to AI production are making this distinction clearly, and building their AI architecture around it.

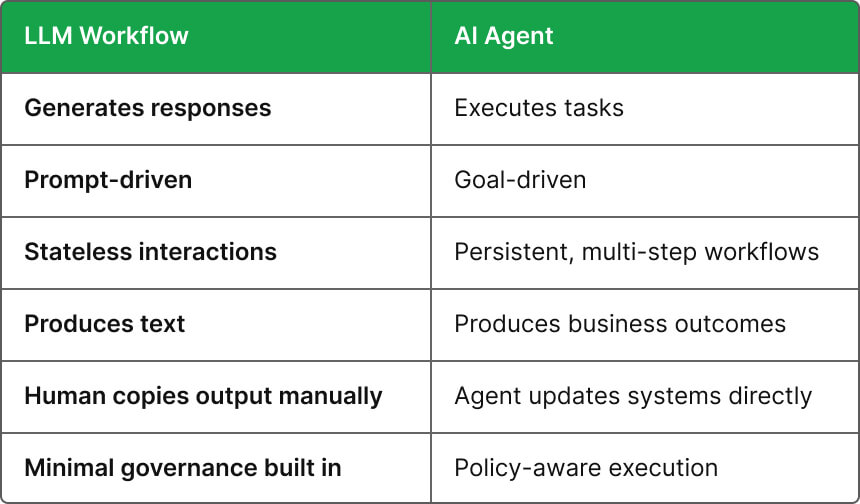

An LLM generates responses. An AI Agent executes work. For financial institutions operating in regulated environments, that difference determines whether AI produces value or just produces outputs.

A large language model workflow follows a consistent pattern: receive a prompt, retrieve relevant context, generate a text response, return it to the user. The user then decides what to do with it.

This pattern is genuinely useful for a significant category of knowledge work. Summarizing a lengthy document before a meeting. Answering an employee's question about a policy. Drafting an initial response to a client inquiry. Generating a first-pass outline of a report that a professional will then revise. For these tasks, where the output is content that a human reviews and acts on, LLM workflows deliver real productivity improvement.

The limitation surfaces when the task requires the AI to not just generate content but to complete a workflow: retrieve specific data from a system, apply a defined set of rules to it, produce a structured output in a specified format, validate that output against policy, route it to the right person, and update a record to reflect that the task was completed. At this point, a prompt and a text response are the wrong tool. The task requires execution infrastructure, not content generation.

The practical distinction: If the next step after the AI produces an output is a human copying it into a system manually, the workflow has not been automated. It has been assisted. That is valuable, but it is not the operational leverage that financial institutions are looking for.

An AI agent does not just generate content; it executes tasks. The distinction is architectural. An agent can retrieve data from external systems, call APIs, apply decision logic, validate outputs against defined rules, route exceptions to human reviewers, update records, and maintain state across a multi-step workflow that may span hours or days.

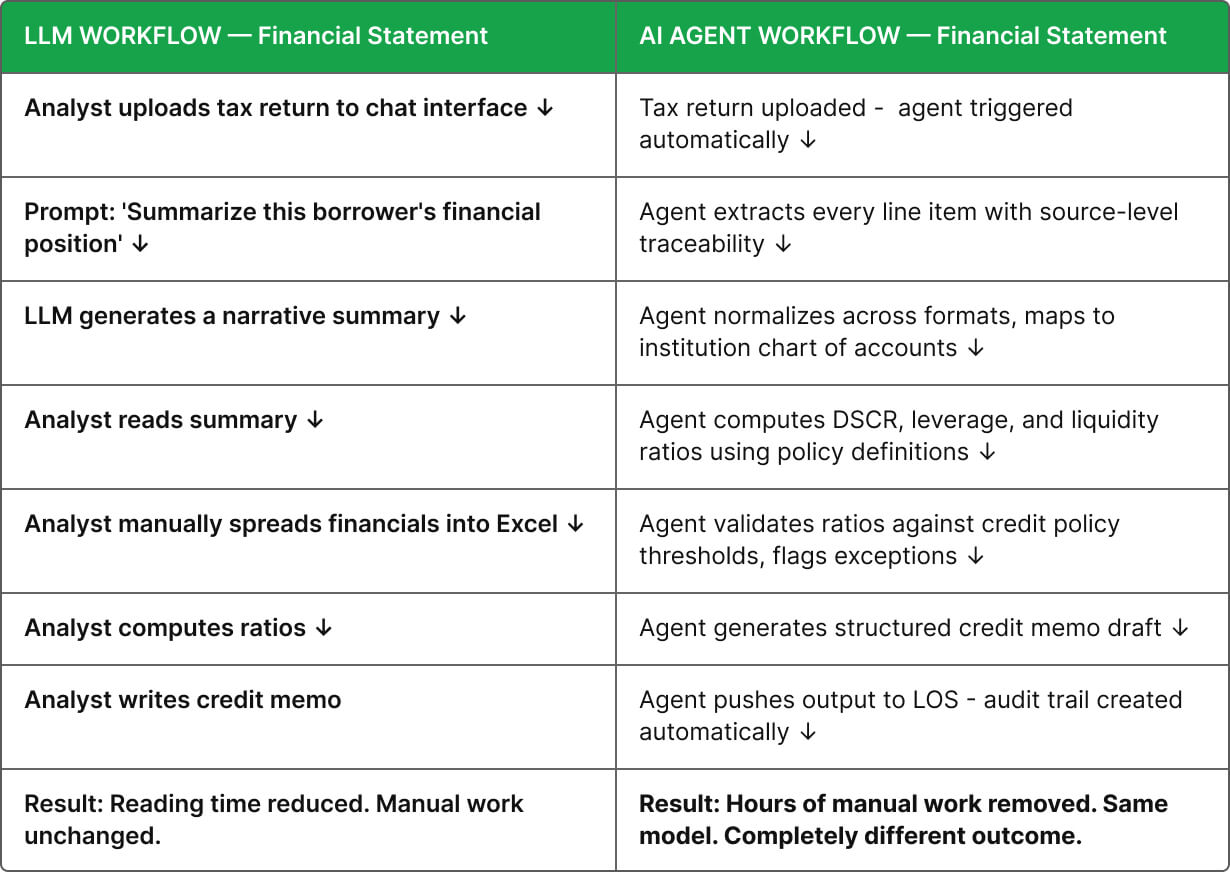

In a financial services context, that means an agent can take a borrower's uploaded tax returns and not just summarize them, it can extract every relevant line item, normalize the data across formats and fiscal periods, map it to the institution's chart of accounts, compute DSCR and leverage ratios using policy-aligned definitions, validate the outputs against credit thresholds, draft the credit memo, and push the structured result into the LOS, all as a continuous, governed workflow with a complete audit trail.

The underlying language model may be the same one generating the summary in the LLM workflow scenario. What differs is the infrastructure around it: the orchestration layer that sequences the tasks, the integrations that connect to external systems, the policy controls that constrain outputs to compliant parameters, and the governance framework that ensures every step is logged, explainable, and subject to human review.

The architectural distinction: LLM workflows and AI agents can use the same underlying model. The difference is the execution infrastructure around it, orchestration, integrations, policy controls, governance, and audit trails. That infrastructure is what determines whether AI produces an output or completes a workflow.

Financial institutions operate in an environment where the output of any AI workflow may be scrutinized by a regulator, evaluated by a credit committee, or used as the basis for a consequential decision affecting a borrower. This environment creates requirements that LLM workflows, by design, are not built to meet.

A complete picture requires acknowledging where LLM workflows are the right tool. The use cases where they excel, and where financial institutions should continue using them, are those where the output is content for human consumption rather than inputs to a downstream workflow.

These are productivity tools. They are worth deploying, and they deliver real value. The important distinction is that they are not operational automation; they assist human work rather than completing it. When the goal is to remove manual work from a lending workflow entirely, rather than helping a human do it more efficiently, the right architecture is an agent, not a prompt.

The language model capability is present in both workflows. What differs is the orchestration, integration, policy enforcement, and governance infrastructure around it. That infrastructure is the difference between a tool that helps people work and a system that does the work.

Three years ago, access to a capable AI model was a competitive advantage. Today, every financial institution and every vendor selling to them has access to models that are powerful enough to generate accurate, fluent outputs across a wide range of tasks. The model is no longer the differentiator.

The differentiator is what surrounds the model: the orchestration layer that sequences multi-step workflows, the integrations that connect AI outputs to the systems they need to update, the policy controls that constrain AI behavior to institutional rules, the governance framework that produces audit-ready outputs as a byproduct of normal operation, and the reusable skill library that allows proven capabilities to be deployed across new workflows without being rebuilt from scratch.

This is the last mile of AI in financial services, the gap between what a model can generate and what a regulated institution can deploy in production. Closing that gap is an infrastructure problem, not a model problem. And it is the reason that the competitive advantage in financial AI belongs not to the organizations with the most advanced models, but to those with the most capable execution infrastructure.

The QORE framework: Rather than deploying standalone LLMs, production-grade financial AI composes specialized agents from reusable financial skills, workflow orchestration, policy-aware execution, API integrations, and governance controls, enabling institutions to automate governed financial work rather than simply generating content.

Use this framework when evaluating whether a proposed AI deployment is an LLM workflow or production-grade agent infrastructure:

✓ Can it integrate with our LOS, CRM, and core banking systems, or does a human have to copy outputs into those systems manually?

✓ Can it execute multi-step workflows autonomously, or does each step require a new prompt and human direction?

✓ Does every output carry source-level data lineage traceable to the originating document and line item?

✓ Can the institution's specific credit policies be embedded in the workflow logic, or is the model applying generic defaults?

✓ Does the system maintain an immutable audit trail of every action, output, and human review, available for examination?

✓ Can it route exceptions to human reviewers automatically, and are those reviews logged?

✓ Is human override available at every output, and is it structurally required before consequential decisions are made?

An AI product that cannot answer yes to these questions is an LLM workflow. It may be useful for productivity. It is not production-grade operational infrastructure for a regulated financial institution.

Rather than deploying standalone LLM interfaces, QORE composes specialized financial AI agents from reusable financial skills, workflow orchestration, policy-aware execution logic, and API integrations, creating governed, audit-ready workflows that execute operational work rather than generating content for humans to act on.

The Intake Superagent does not summarize incoming documents. It classifies them, validates completeness, triggers KYC and KYB verification in parallel, and assembles a structured loan file with a complete chain of custody. The Underwriting Superagent does not describe a borrower's financial position. It extracts, normalizes, and computes it, using the institution's policy definitions, and produces a structured output with source-level traceability on every figure. The Continuous Monitoring Superagent does not alert a relationship manager that something might be wrong. It calculates the specific covenant ratio that has deteriorated, identifies the threshold it is approaching, and surfaces the exception with supporting data.

Every capability is governed by the institution's credit policies, integrated with existing lending infrastructure, and auditable at the level of detail regulators require. The goal is not AI that produces impressive outputs. It is AI that completes regulated financial workflows safely, consistently, and at scale.

The financial institutions that will build durable competitive advantage through AI are not the ones that have deployed the most impressive language model demonstrations. They are the ones who have built or deployed the execution infrastructure that allows capable models to operate in production: governed, integrated, policy-aware, and audit-ready.

LLM workflows are a legitimate productivity tool. They belong in knowledge work applications where the output is content for human consumption. They are not the right architecture for the regulated, multi-step, system-integrated operational workflows that define financial services.

The future of financial AI will be determined by which organizations can reliably execute regulated workflows, integrate with existing systems, and deliver explainable outcomes at scale. That is the difference between an LLM workflow and an AI agent, and it is the difference that determines whether AI produces content or creates operational value.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.