July 2, 2026

Why Workflow Automation Tools Fail in Lending

Lending

The lending industry has never been short of innovation. New credit models, smarter risk frameworks, and broader capital access. The industry has spent decades getting better at the fundamentals.

But here's what nobody planned for.

All that progress in credit sophistication is now running into a different kind of wall. Not a capital problem. Not a demand problem. But an operational problem.

Non-bank financial institutions are scaling into markets that their infrastructure simply wasn't built for. For Private credit, equipment finance, and specialty lending, volumes are growing, deal complexity is rising, and governance expectations keep tightening. Yet the systems running underneath most lending operations haven't kept pace. Fragmented workflows create friction. Manual processes inflate costs. Rigid technology stacks slow down the decisions that need to happen fast.

The result is a gap that widens quietly. Until growth stalls and the real culprit turns out to be the operational model itself.

That's the realization driving a fundamental shift across the industry. Not process tweaks or tool upgrades, but a full redesign of how lending operations are built, with AI automation at the center of it.

Most non-bank financial institutions didn't set out to build a patchwork of tools. It just happened that way.

A loan origination system here. Document management tools there. Spreadsheets for analysts, email chains for collaboration, separate platforms for compliance and reporting. Each tool solved a specific problem at the time. Together, they created something harder to manage. The fragmented workflows create friction at every stage of the lending lifecycle.

The challenges that come with this are predictable.

Firstly, information is scattered across systems, so maintaining a single source of truth becomes a daily battle. Analysts spend significant chunks of their time reconciling documents, validating financial information, and updating data across platforms that don't talk to each other.

Secondly, manual handoffs between intake teams, analysts, credit committees, and closing teams slow everything down.

Thirdly, rigid rule-based systems, the kind that work perfectly in controlled conditions, struggle the moment real-world lending complexity enters the picture. Exceptions pile up. Human intervention steps in. Delays follow.

On their own, these inefficiencies can feel manageable. At scale, they compound fast. For institutions processing hundreds or thousands of deals, operational friction doesn't just slow things down, it inflates costs and stretches decision cycles in ways that become genuinely hard to recover from.

Operational inefficiencies in lending have a habit of staying invisible, right up until a firm tries to grow.

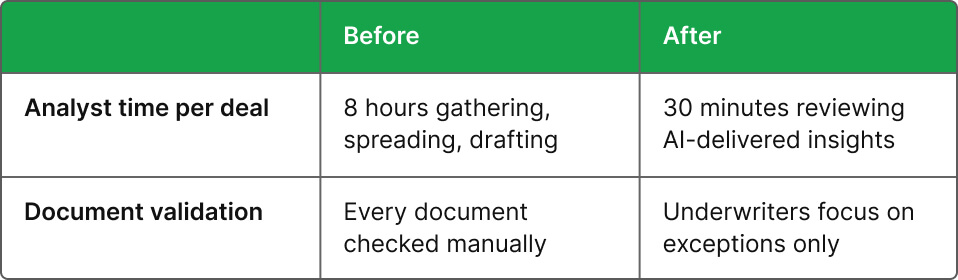

Manual processes add time to every step: processing applications, performing financial analysis, drafting credit memos, and finalizing documentation. Analysts spend hours extracting data from financial statements or cross-checking borrower information across multiple documents. It's work that needs to get done, but it's work that shouldn't require a skilled analyst to do it.

Over time, this creates structural challenges that go beyond day-to-day frustration.

Deal cycles stretch out. When workflows depend on human intervention at multiple stages, loan processing timelines expand at every one of them. Delays accumulate during document collection, underwriting analysis, internal approvals, and compliance verification, often without anyone realizing how much time is being lost.

Operational costs climb. As deal volumes grow, the natural response is to hire. More analysts, more operations staff. It works in the short term, but it's an expensive way to scale, and it doesn't fix the underlying problem.

Scalability hits a ceiling. Legacy systems weren't built to handle rapid growth in deal volume or complexity. So operational capacity tends to grow in a straight line with headcount, rather than scaling with the business.

Governance becomes harder to manage. When workflows span multiple disconnected systems, maintaining consistent compliance, auditability, and policy enforcement becomes a genuine challenge, not just an administrative one.

In competitive markets like private credit and equipment finance, these inefficiencies don't stay operational problems for long. They become strategic ones.

AI delegation isn't a shinier version of automation. It's a fundamentally different concept.

Automation executes predefined steps. Delegation actually performs parts of the work itself.

Instead of simply routing an equipment lease application to an analyst, AI systems now:

AI moves from workflow facilitator to analytical collaborator. What that looks like in practice:

AI delegation doesn't replace lending expertise. It eliminates the repetitive analytical grind, consuming it, freeing professionals for the higher-value judgment that actually moves the needle. Underwriting capacity has doubled without headcount growth across 150+ lending operations.

The AI-automated lending operating model that's emerging isn't a single tool or a single fix. It's a set of components that work together to make operations genuinely scalable.

AI systems collect borrower information, analyze uploaded documents, and structure financial data automatically, removing the need for manual document verification and data entry before underwriting even begins.

AI tools process financial statements, bank statements, and other records to generate structured insights that support underwriting decisions. What used to take analysts hours now happens in minutes.

Workflow orchestration replaces the manual handoffs that slow everything down. AI-driven workflows route deals between teams automatically based on predefined policies, so nothing gets stuck waiting for someone to forward an email.

AI systems can ensure that policies are applied consistently, while maintaining audit trails for regulatory or internal compliance requirements.

When these components work together, lending operations stop depending on individual teams to push deals forward manually. The system handles workflow progression. Teams focus on the decisions that actually require human judgment.

The shift toward AI-automated lending infrastructure is already producing measurable outcomes for the institutions that have made it.

And perhaps most importantly, the business becomes genuinely scalable. As lending volumes grow, AI-driven workflows handle the increasing workload without requiring significant changes to operational structures underneath.

The lending industry is entering a phase where operational design will matter as much as credit expertise in determining who comes out ahead.

For many non-bank financial institutions, the challenge has already moved past access to capital or borrower demand. The real question now is whether operations can keep up, whether deals can be processed efficiently, governance can be maintained, and the business can scale without operational costs eating into the returns that made it worth building in the first place.

Traditional lending infrastructure wasn't designed for this environment. AI automation offers a genuine path forward, not by patching existing systems, but by enabling institutions to redesign operations from the ground up around intelligence, automation, and embedded governance.

The institutions that make this shift thoughtfully and early will be better positioned to compete on speed, cost, and operational reliability as lending markets keep growing. Those who wait will find the gap harder to close than they expected.

The blueprint is here. The question is whether you're ready to use it.

See how Uptiq redesigns lending operations from the inside. Book a demo and find out how much capacity your team is leaving on the table.

AI automation in lending refers to the use of artificial intelligence to automate operational processes across the lending lifecycle, document extraction, financial analysis, underwriting support, workflow management, and compliance monitoring.

To reduce operational costs, speed up lending decisions, and improve scalability. AI systems handle repetitive tasks and complex data processing, freeing lending teams to focus on higher-value analysis and decision-making.

By processing documents, extracting financial data, and coordinating workflow transitions automatically, removing the delays caused by manual data entry, document verification, and internal handoffs.

Yes, AI systems embed policy rules directly into lending workflows and maintain detailed audit trails for decisions and approvals, improving transparency and supporting both regulatory and internal governance requirements.

Borrower intake, document analysis, financial data extraction, underwriting support, credit memo preparation, workflow management, and closing coordination can all be supported through AI automation.