June 20, 2026

Risks of Using AI in Lending (Compliance, Bias & Auditability)

When AI enters a conversation about credit decisioning, the instinct in most lending institutions is to frame it as a replacement question. Will AI replace the rule engine? Will it override credit policy? Will automated decisioning remove the governance structures that regulators expect to see?

These concerns are understandable, but they rest on a false premise: that AI and rule-based systems are competing for the same role in the credit workflow. They are not.

Rule engines define and enforce credit policy. They evaluate whether a borrower meets predefined criteria: DSCR thresholds, credit score floors, debt ratio limits, and route the application accordingly. That function is not going away. It should not go away. It is precisely what makes credit decisions consistent, explainable, and defensible under examination.

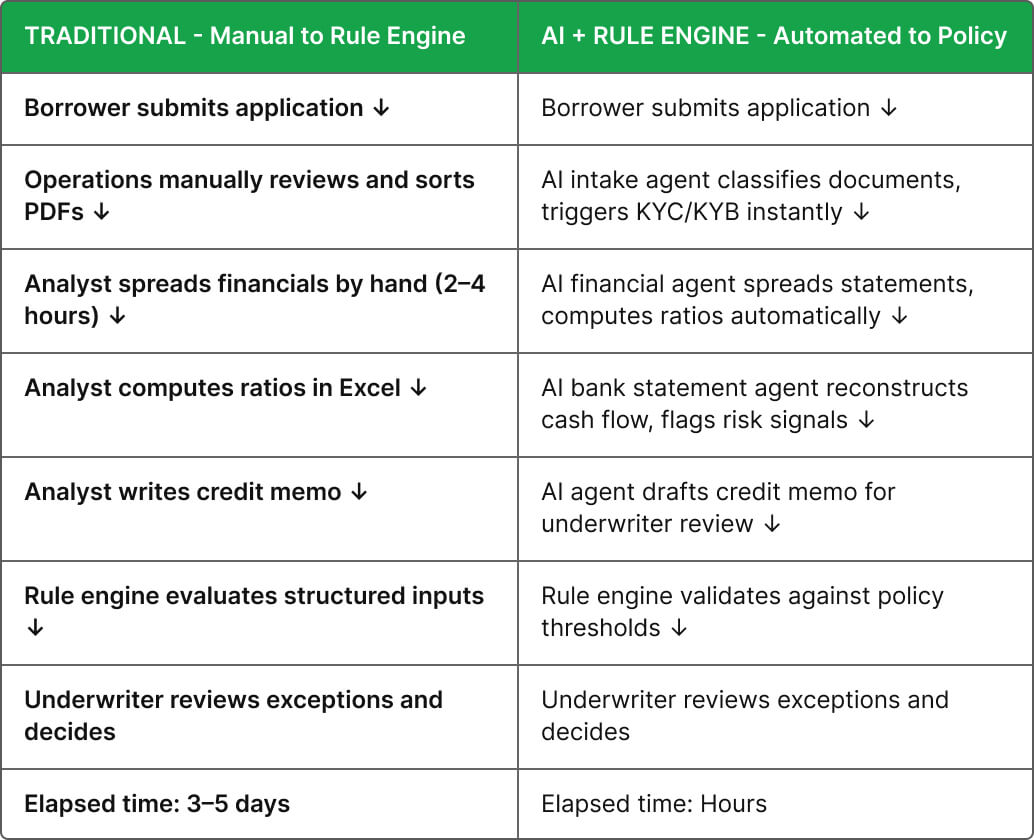

What AI adds to this architecture is something different: the ability to automate the operational work that currently happens before the rule engine ever sees the application. Document extraction, financial spreading, cash flow analysis, credit memo generation, policy exception flagging, all of it happens manually today, by analysts whose time would be better spent on the judgment that no rule engine can replicate.

The question isn't AI or rules. It's how AI can execute operational workflows so that rules can do their job faster, on better information, with less manual effort in between.

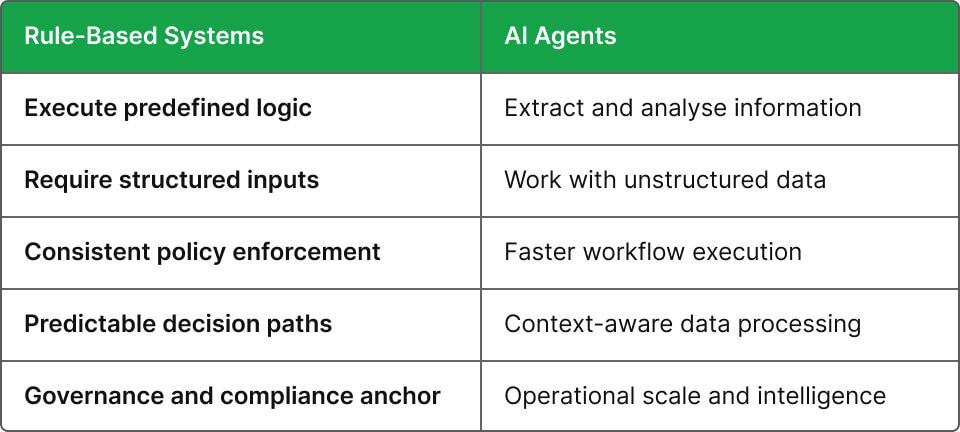

A rule-based credit decisioning system evaluates loan applications against a set of predefined logical conditions, eligibility criteria, risk thresholds, policy parameters, and regulatory requirements, and produces a consistent output based on whether those conditions are met.

A simplified example of what that logic looks like in practice:

IF DSCR > 1.25 AND Credit Score > 700 AND Debt Ratio < 45% → Eligible for Approval

Rule engines are valuable precisely because they are predictable, consistent, and explainable. The same application evaluated twice produces the same output. Policy is applied uniformly across every decision. Examiners can trace exactly why a decision was made and verify that it was policy-compliant.

Their limitation is the input they require: structured, validated data. A rule engine cannot read a PDF tax return. It cannot interpret three months of bank transactions. It cannot reconstruct cash flow from a set of inconsistently formatted financial statements. It needs clean, structured numbers, and producing those numbers has always been the manual work that sits upstream of the rule engine itself.

AI does not compete with the rule engine. It feeds it. The role of finance-native AI agents in credit decisioning is to transform the unstructured, high-volume operational work that precedes policy evaluation into the clean, structured inputs that rule engines are designed to receive.

In practice, that means:

Every one of these tasks produces structured output that the rule engine and the underwriter can immediately use. AI does not make credit decisions. It creates the conditions under which credit decisions can be made faster, with more complete information, and with less manual effort in between.

The most useful way to understand the difference between AI and rule-based systems is not as a competition but as a division of labor, each one doing the work it is designed for:

The architecture insight: Rule engines provide governance; they ensure every decision reflects credit policy consistently and traceably. AI agents provide operational scale; they ensure the rule engine receives structured, validated inputs without requiring hours of manual work to produce them. The two are complementary by design.

Rule engines are the right tool for any part of the credit workflow that requires consistent policy application, regulatory traceability, and predictable output. This includes eligibility checks against defined criteria, approval routing for applications that clearly meet or miss policy thresholds, exception flagging for deals that require escalation, and compliance documentation that demonstrates policy was applied uniformly.

These are precisely the governance functions that regulators evaluate. A rule engine that applies the same logic to every application provides the audit trail and decision consistency that examination requires. Replacing or weakening this layer in the name of AI flexibility would be the wrong trade.

AI creates value in the operational layer that sits upstream of policy evaluation, and in the monitoring layer that sits downstream of it. Before the rule engine can evaluate an, application, someone has to produce the structured financial metrics it needs. That work, document intake, financial spreading, cash flow analysis, memo preparation, is where AI agents deliver the most measurable operational impact.

Post-close, AI monitoring agents re-spread borrower financials continuously, calculate updated covenant ratios, and surface exceptions to the portfolio manager when they occur rather than weeks later. The rule engine defines the covenant thresholds; the AI agent watches them continuously.

The institutions gaining the most ground in lending operations are not choosing between AI and rule engines. They are deploying both, in sequence, with each doing the work it is designed for.

The rule engine provides governance: consistent policy application, regulatory traceability, and audit-ready decision documentation. AI provides execution: structured inputs delivered faster, with greater analytical depth, without consuming analyst capacity in the process. Together, they produce underwriting cycle times 40–50% shorter than manual processes achieve, with output that is more consistent, more complete, and more defensible.

The integration question - how do AI agents connect to the existing rule engine infrastructure, is addressed through the same approach that governs the rest of the deployment: agents layer over existing systems rather than replacing them. The LOS, the rule engine, and the core banking platform stay in place. The AI agents add the operational intelligence layer that feeds them.

MISCONCEPTION: AI makes credit decisions automatically.

REALITY: AI prepares structured information and flags policy exceptions. The credit decision remains with the underwriter and the rule engine. AI does not approve or decline applications , it creates the conditions under which humans and policy rules can do so faster.

MISCONCEPTION: AI replaces the need for rule engines.

REALITY: Rule engines are the governance layer that ensures policy is applied consistently and traceably across every decision. AI agents are the operational layer that produces the inputs those rule engines need. Removing the rule engine would remove the policy enforcement mechanism that regulators require.

MISCONCEPTION: AI-driven credit analysis cannot be audited.

REALITY: Finance-native AI agents produce outputs with full data lineage, every ratio traceable to the source document, every categorization explainable, every workflow step logged. The audit trail produced by a well-designed AI deployment is more complete than the documentation produced by manual processes.

Uptiq deploys finance-native AI agents that operate in the workflow layer upstream of policy evaluation: automating document intake, financial spreading, bank statement analysis, credit memo generation, and portfolio monitoring while applying the institution's existing credit policies consistently at every step.

The Intake Superagent handles document classification and KYC/KYB orchestration. The Underwriting Superagent manages financial spreading, ratio computation, and credit memo generation. The Continuous Monitoring Superagent tracks covenant compliance and surfaces exceptions continuously post-close. All agents integrate with existing LOS, core banking systems, and rule engines, no replacement required.

Every output is explainable, source-traced, and policy-aligned. The rule engine receives clean, validated inputs. The underwriter receives a structured, decision-ready analysis. The governance layer remains exactly where it should be: in the rule engine and in the professional judgment of the credit team.

On integration: Uptiq agents connect to existing rule engines and LOS infrastructure. The credit policy stays in the rule engine. The operational execution moves to the agents.

The conversation about AI versus rule-based systems in lending has been framed as a competition for too long. In practice, the institutions deploying AI most effectively are not replacing their rule engines. They are pairing them with AI agents that do the operational work the rule engines cannot, handling unstructured documents, extracting structured data, computing financial metrics, and drafting credit narratives, so that the rule engine receives the inputs it needs to do its job faster and more consistently.

Rules provide policy. AI provides execution. Together, they produce credit decisions that are faster, more consistent, and more explainable than either can deliver operating independently.

The future of credit decisioning is not AI replacing rules. It is AI executing the operational work surrounding those rules, so lending teams can apply policy faster, with better information, and without the manual effort that has always slowed the process down.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.