July 2, 2026

Why Workflow Automation Tools Fail in Lending

A Practical Playbook With Uptiq’s Client Lending Platform

In the modern lending landscape, speed matters. Borrowers don’t want to wait days, let alone weeks, for loan decisions. Yet traditional lending processes are notorious for bottlenecks caused by:

For advisors, this friction isn’t just an operational annoyance, it directly impacts client satisfaction, approval rates, and loan funding velocity.

Enter AI-powered lending platforms like Uptiq’s Client Lending Platform. These tools help advisors prepare borrowers for faster approvals by automating document intelligence, risk assessment, and lender matching, while ensuring accuracy and compliance.

This guide walks loan advisors through a complete process for preparing borrowers using AI, so loans get approved quickly and efficiently.

Before diving into solutions, it’s important to recognize common causes of slow approvals:

Borrowers often submit:

Each missing document adds days to processing.

Underwriters spend most of their time reading and re-reading documents instead of evaluating risk.

Borrowers send information in different formats, PDFs, pictures, spreadsheets, without consistency.

Many lenders rely on email threads or phone calls to clarify missing items, leading to time delays and lost context.

AI tools, particularly those designed for lending, automate painful and repetitive tasks:

AI reads ANY uploaded document, regardless of format, classifies it, and extracts key fields.

From bank statements to tax forms, AI pulls out relevant values like revenue, cash flow, debt balances, net worth, etc.

AI flags inconsistencies, missing pages, mismatches, and potential fraud indicators automatically.

Before the underwriter even opens a file, AI suggests:

This drastically reduces review time.

Uptiq’s Client Lending Platform is built around this core capability, empowering advisors and lenders with AI-driven readiness insights that speed approvals.

Here’s a practical playbook advisors can follow:

Before advisor-borrower meetings, ask borrowers to upload:

AI tools like Uptiq automatically recognize these files and extract financial metrics such as:

This eliminates manual data entry.

Required forms may include:

Uptiq’s AI reads and extracts line-by-line items in these forms, no need for manual review.

This helps advisors:

Borrower readiness isn’t just about numbers, it’s also about integrity, credibility, and underlying risk.

Collect:

AI analyzes these and surfaces:

Faster background verification means fewer surprises during underwriting.

If the loan requires collateral, have borrowers upload:

Uptiq’s Document AI extracts:

This allows advisors to pre-qualify collateral strength with confidence.

Uptiq automatically:

This completeness check is vital:

Advisors don’t send incomplete files to underwriters.

AI ensures submissions are:

Accelerating approvals without rework.

Once documents are ingested, advisors can see:

This allows advisors to proactively adjust:

Before underwriters even touch the file.

AI insights are not just for underwriting, they empower advisors to coach borrowers too.

This builds trust and increases approval likelihood.

AI highlights missing documents instantly.

Solution: Upload reminders + completeness dashboards.

Manual forecasting is error-prone.

Solution: Uptiq’s AI extracts historical cash flow and projects trends.

Advisors often juggle spreadsheets.

Solution: Uptiq models different loan structures automatically.

Back-and-forth communication kills momentum.

Solution: AI-verified files reduce underwriter clarifications.

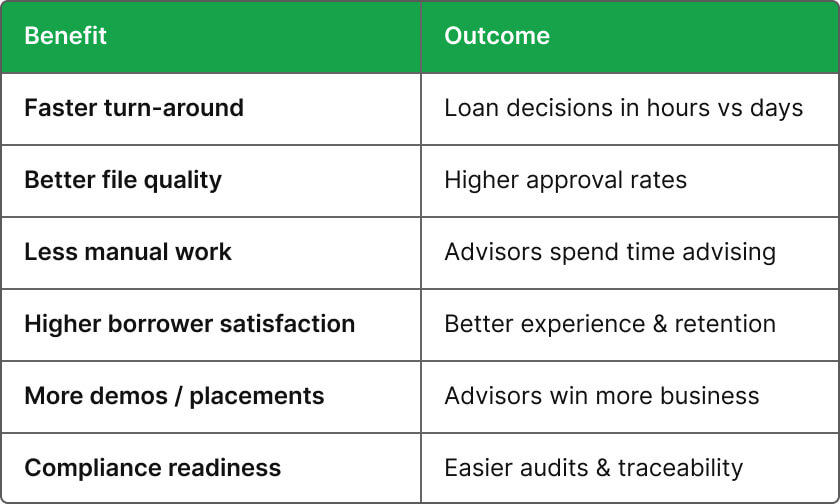

Using AI tools upstream leads to real business impact:

Underwriters move from data entry to decision strategy.

Loan terms adapt to real-time cash flow.

Interest & margins tailored to risk signals.

Borrowers apply directly inside partner apps with instant AI support.

Preparing borrowers for faster approvals isn’t just a tactical improvement, it's a strategic advantage.

With Uptiq’s Client Lending Platform, advisors can:

AI tools don’t replace advisors, they empower them to be more effective, accurate, and trusted.

If you’re ready to take borrower preparation to the next level, it starts with adoption of intelligent lending tools like Uptiq.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.