June 20, 2026

Risks of Using AI in Lending (Compliance, Bias & Auditability)

Most conversations about AI in lending start in the wrong place. They lead with what the technology can do: process documents faster, score credit automatically, surface risk signals, rather than asking a more grounded question: where does the operational time in a lending team actually go?

The answer, at most banks, credit unions, and non-bank lenders, is not where people assume. Credit judgment, the evaluation of risk, the application of policy, and the decision itself are often the smallest portion of an underwriter's day. The majority of their time goes to the operational work that surrounds that judgment: collecting documents, spreading financials, reviewing bank statements, writing memos, updating systems, chasing exceptions.

That is the problem AI in lending is built to solve. Not to automate credit decisions, but to automate the operational work that currently consumes the capacity of the people making them. The goal is not to replace lenders. It is returning their time to the work that requires their expertise.

AI in lending is not one tool. It is a collection of specialized agents that automate specific lending workflows while keeping humans in control of every decision.

AI in lending uses intelligent automation to perform the repetitive, high-volume operational tasks that currently consume underwriting and credit operations capacity, document processing, financial analysis, underwriting support, and portfolio monitoring with consistent accuracy and without requiring manual effort at each step.

The distinction worth making upfront is between AI that assists and AI that operates. Assistive AI: copilots, chatbots, and summarization tools help analysts work faster on tasks they are already doing. Operational AI, like the specialized agents designed for specific lending workflows, removes those tasks from the analyst's workload entirely, handling them automatically so the analyst's attention can be directed to work that genuinely requires human judgment.

Most of the measurable value in lending comes from the second category. The agents that automate document intake, financial spreading, bank statement analysis, credit memo generation, and portfolio monitoring are where 40–50% reductions in cycle time come from, not from tools that make the existing manual process marginally faster.

AI does not replace the lending workflow. It operates inside it, at each stage where repetitive, structured work currently consumes analyst capacity that could be directed elsewhere.

INTAKE Application & Document Processing

→ Documents classified and completeness assessed automatically

→ KYC/KYB checks triggered without manual intervention

→ Missing items flagged and borrower follow-up initiated

UNDERWRITING Financial Analysis & Credit Support

→ Tax returns and financial statements spread automatically

→ DSCR, leverage ratios, and liquidity metrics computed instantly

→ Bank statements categorized and behavioral risk signals surfaced

DECISION Credit Memo & Policy Validation

→ Credit memo narrative drafted and formatted automatically

→ Policy thresholds validated and exceptions flagged for review

→ Underwriter reviews structured output and makes credit judgment

POST-CLOSE Portfolio Monitoring & Covenant Tracking

→ Borrower financials re-spread on schedule automatically

→ Covenant ratios updated and breach likelihood scored continuously

→ Exceptions surfaced to relationship managers when they occur

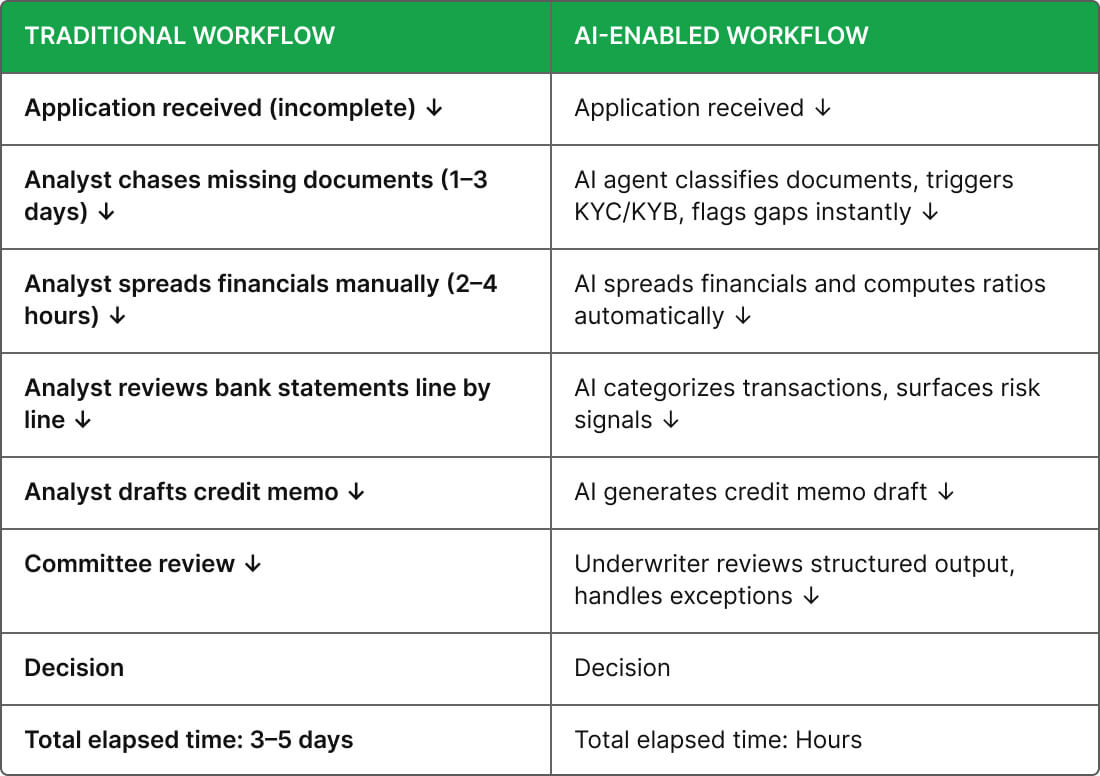

Loan applications rarely arrive complete. An intake agent classifies incoming documents, assesses completeness against a configurable checklist, triggers KYC and KYB verification automatically, and initiates follow-up requests for missing items, all before the underwriter opens the file. The analyst inherits a structured, complete package rather than building it.

Manual financial spreading, i.e. extracting line items from tax returns and CPA-prepared statements, normalizing across formats, computing DSCR and leverage ratios takes two to four hours per deal. A financial analysis agent does this in minutes, applying consistent policy-aligned definitions and producing a structured output with full data lineage traceable to the source document.

An AI agent processes months of bank statement transaction history automatically, categorizing every entry, identifying recurring obligations, flagging NSF patterns, and computing average monthly cash flow and burn rate. The analyst receives a behavioral risk summary rather than a stack of PDFs to scroll through manually. Detection is more complete and more consistent than manual review at volume.

Once the analysis is complete, a credit memo agent drafts the narrative automatically, structuring the policy rationale, embedding the computed ratios, and formatting the output to match the institution's template. The underwriter reviews and approves rather than writing from scratch. Memo preparation time drops from hours to minutes.

A monitoring agent re-spreads borrower financials on a defined schedule, calculates updated covenant ratios, scores breach likelihood against thresholds, and surfaces exceptions to the relationship manager proactively. Quarterly reviews that previously caught risk signals weeks after they became relevant are replaced by continuous monitoring that surfaces them when they occur.

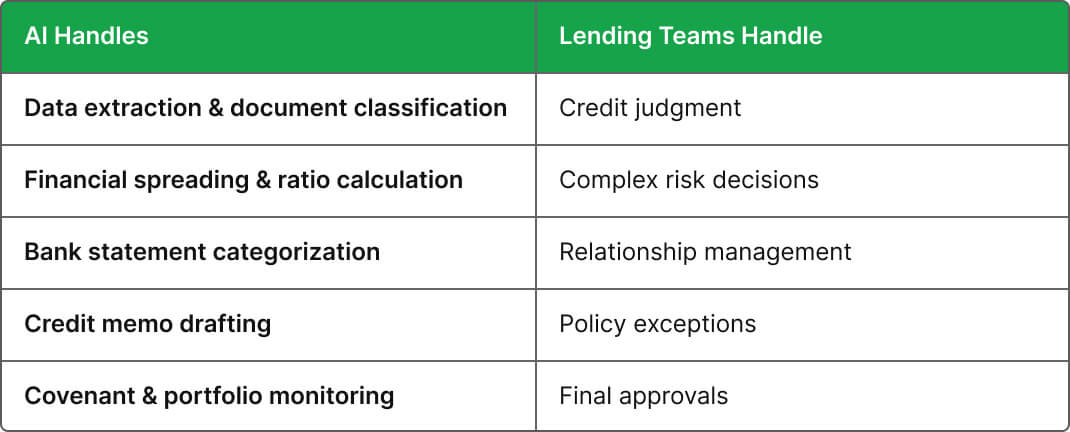

The division of labor between AI agents and lending professionals is where the design of any AI deployment matters most. The answer is straightforward: AI handles the work that is structured, high-volume, and rules-based. Lenders handle the work that requires judgment, context, and accountability.

Every AI output is reviewable, explainable, and overridable. The underwriter remains in control of every credit decision. What changes is the quality and completeness of the analysis the decision is based on, and the hours no longer consumed by producing it manually.

AI deployment in lending is not without real implementation considerations. Addressing them directly is the difference between a pilot that stalls in committee and a deployment that reaches production.

Data quality: AI agents are only as reliable as the data they process. Institutions with inconsistent document collection practices or non-standardized financial templates will need to address those upstream before automation delivers consistent outputs.

Governance and oversight: Every AI-assisted output that influences a credit decision must be reviewable by a qualified human and traceable to its source. Governance should be embedded in the deployment architecture from the start, not added afterward.

System integration: AI agents need to connect to existing LOS, CRM, and core banking systems. Institutions that have not mapped their integration requirements before selecting a vendor consistently discover this is the primary deployment bottleneck.

Explainability: Regulatory expectations require that AI-influenced decisions be explainable in human terms. Finance-native agents with source-level traceability meet this standard; generic AI tools that produce probabilistic outputs without attribution do not.

On governance: The institutions that deploy AI successfully treat governance as a design requirement, not a compliance afterthought. The right architecture makes auditability a byproduct of normal operation — not a separate documentation effort.

The deployment path that consistently produces results is not a broad platform rollout. It is a sequence of targeted deployments, each one demonstrating value in a specific workflow before expanding to the next.

Each deployment builds on the previous one. Each produces measurable results before the next is added. The organization builds confidence in the outputs at each stage, and the governance framework scales incrementally rather than being implemented all at once across a complex multi-workflow deployment.

Uptiq deploys finance-native, pre-trained AI agents across the full lending lifecycle, each one purpose-built for a specific workflow, each one integrated with the LOS, CRM, and core banking systems the institution already uses. No infrastructure replacement. The agents layer over what is already in place.

The Intake Superagent handles document collection, classification, and KYC/KYB orchestration. The Underwriting Superagent manages financial spreading, bank statement analysis, ratio computation, and credit memo generation. The Continuous Monitoring Superagent handles post-close portfolio oversight, re-spreading financials on schedule, scoring breach likelihood, and surfacing covenant exceptions proactively.

The agents work together across the loan lifecycle, sharing data and passing structured outputs between workflow stages. Each one is configurable to the institution's specific credit policies, document templates, and approval thresholds. Every output is explainable, source-traced, and audit-ready.

On integration: Uptiq connects to existing systems rather than replacing them. The first workflow deployment typically goes live within weeks, not months.

AI in lending is not a single technology or a universal platform. It is a set of specialized agents, each one designed for a specific stage of the lending workflow, each one removing manual work that should never have required professional expertise in the first place.

The institutions that are realizing the most value from AI are not the ones that deployed the most ambitious system. They are the ones that started with the most pressing bottleneck, demonstrated measurable impact, and expanded from a foundation of operational confidence rather than theoretical potential.

AI in lending is not about automating credit decisions. It is about automating the operational work surrounding those decisions, so lending teams can process more applications, make faster decisions, and scale their operations without scaling the manual effort that has always come with them.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.