June 20, 2026

Risks of Using AI in Lending (Compliance, Bias & Auditability)

Ask your underwriters what they did yesterday.

The answer is rarely 'I made credit decisions.' More often, it sounds like: chased a borrower for missing tax returns, rebuilt a financial spread from a PDF, manually categorized bank transactions in Excel, formatted the credit memo to match the template, and updated the LOS before the 5 pm cutoff.

The credit judgment, the part that requires their expertise, their experience, and their professional accountability, typically occupies a fraction of the day. Everything around it is administrative work that happens to require a credentialed professional because no one has automated it yet.

The fastest underwriting teams are not faster because their analysts are sharper. They are faster because they have systematically removed the administrative layer from the analyst's workload. The judgment stays. The assembly work goes.

Underwriting isn't slow because of credit analysis. It's slow because of everything that has to happen before credit analysis can begin.

Most underwriting operations have never formally mapped where cycle time is spent. When teams do, the distribution is consistently surprising. The credit judgment itself, the evaluation of risk, the application of policy, and the decision represent a relatively small portion of the total elapsed time. The rest looks like this:

The pattern: At most commercial lending operations, 60–70% of the underwriting cycle time is consumed by work that does not require credit judgment. It requires data assembly, document processing, and administrative coordination.

Document intake is still largely manual at most lenders. Files arrive through email, broker portals, and direct submission, in different formats, with inconsistent completeness. Someone has to classify each document, identify what is missing, and chase the gaps before the underwriter can open. This is not a skill problem. It is a workflow design problem.

Spreading a three-year tax return package for a multi-entity borrower, manually extracting the right line items, normalizing across formats, calculating DSCR and leverage ratios, and validating the output is two to four hours of structured data entry. It is also the single largest driver of inconsistency across analysts, because each brings slightly different interpretations to the same inputs.

Manually reviewing months of transaction history at the line-item level is where volume most directly translates into quality degradation. Analysts reviewing their eighth bank statement of the day are not performing the same analysis as they did on their first. The patterns that matter - overdraft clustering, undisclosed debt service, revenue volatility- require sustained attention that the volume does not support.

A completed spread does not automatically become a credit memo. Formatting the narrative, structuring the policy rationale, embedding the computed ratios, and aligning the output with the template takes meaningful time. At high deal volume, memo preparation alone can represent 20–30% of total cycle time per deal.

Deals that fall outside standard parameters move through manual escalation sequences with no automated tracking. The deal sits in a queue. Someone follows up. It moves. The elapsed time between exception identification and resolution adds days to the cycle without any productive work occurring in between.

The lenders achieving 40–50% reductions in underwriting cycle time are not doing it by running analysts harder or investing in better spreadsheet templates. They are removing the manual bottlenecks entirely, replacing each one with an AI agent designed to perform that specific workflow accurately, consistently, and without consuming analyst capacity.

Rather than waiting for analysts to classify and chase documents, intake agents process submissions the moment they arrive. Documents are classified automatically. Missing items are identified, and follow-up requests are triggered without human intervention. By the time the underwriter opens the file, it is complete and organized, not a queue of documents waiting to be sorted.

Finance-native AI agents extract line items from tax returns, CPA-prepared statements, and operating financials directly — normalizing across formats, computing DSCR, leverage ratios, and liquidity metrics using policy-aligned definitions, and producing a structured spread with full data lineage. The analyst receives a verified analysis rather than a stack of documents to process. Spreading time drops from hours to minutes.

Rather than requiring analysts to scroll through transaction logs, AI agents categorize every transaction automatically, identifying revenue patterns, flagging NSF activity, surfacing recurring obligations that may represent undisclosed debt service, and computing average monthly cash flow and burn rate. The analyst reviews a structured behavioral summary rather than raw transaction data. The analysis is more complete and more consistent than manual review at volume.

Once the spread and analysis are complete, AI agents draft the credit memo narrative automatically, structuring the policy rationale, embedding the computed ratios, and formatting the output to match the institution's template. The underwriter reviews, edits where professional judgment requires, and approves. What previously took one to two hours takes minutes.

Standard deals that fall clearly within policy parameters move through the workflow with minimal analyst intervention. Exceptions are flagged and routed automatically. Underwriters focus their attention on the deals that genuinely require judgment: complex structures, borderline credits, relationships with contextual nuance. Low-risk processing work is automated. High-judgment work is concentrated.

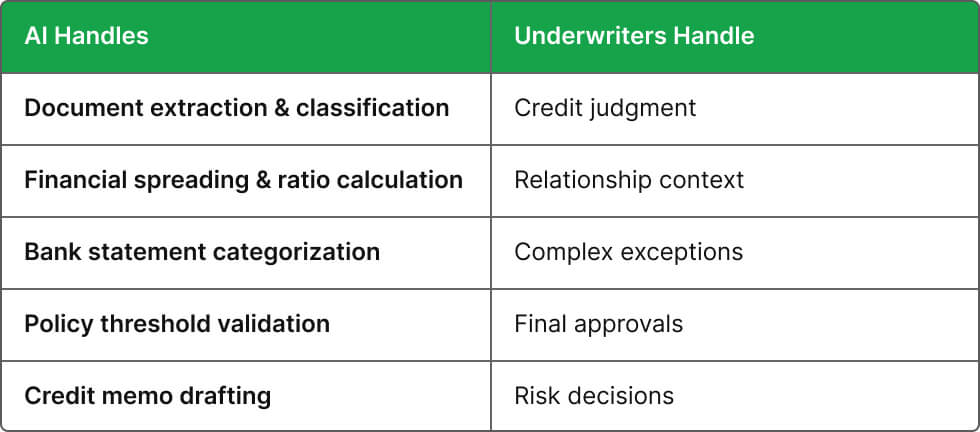

The distinction that matters most in any conversation about underwriting automation is not how much work AI can do. It is what work AI should do. The answer is straightforward:

This division of labor is not a compromise. It is the design. AI agents handle the computational, administrative, and data assembly work, at which they are more accurate, more consistent, and more scalable than human review. Underwriters retain full control of the work that requires professional judgment, relationship context, and institutional accountability.

Two underwriting operations. Same credit standards. Very different cycle times.

Total elapsed time: Hours

Cycle time reduction is the most visible outcome. It is not the only one that matters.

Uptiq deploys finance-native AI agents across the underwriting workflow, each one designed for a specific task and each one integrating with the LOS, CRM, and core banking systems the institution already uses. No infrastructure replacement. No migration.

The Intake Superagent handles document collection, classification, and KYC/KYB orchestration. The Underwriting Superagent manages financial spreading, ratio computation, bank statement analysis, and credit memo generation. Agents operate within the institution's existing credit policy; the outputs are policy-aligned, fully explainable, and traceable to the source.

The underwriter remains in control of every credit decision. What changes is the quality and completeness of what the decision is made with, and the hours reclaimed from administrative work that was never the best use of the analyst's expertise in the first place.

On integration: Uptiq layers over existing systems: LOS, CRM, core banking platforms. Nothing is replaced. The agents connect what is already there and add the intelligence layer that coordinates it.

A 40–50% reduction in underwriting cycle time is not produced by compressing the credit judgment. It is produced by removing the hours of administrative work that currently sit between document receipt and the moment when professional judgment can finally be applied.

The underwriting team you have is capable of handling more volume, making more consistent decisions, and delivering faster responses to borrowers without additional headcount. The constraint is not their expertise. It is the amount of that expertise currently absorbed by work that AI agents can execute more accurately, more consistently, and without the fatigue and variation that volume introduces into manual workflows.

The goal is not to replace underwriters. It is ensuring they spend their time on credit decisions, not on the spreadsheets, documents, and administrative coordination that surround them.

Join more than 140 banks and financial institutions that are using Uptiq's AI agents to automate underwriting, financial spreading, covenant monitoring, document collection, credit intake, and credit memo generation. The future of banking is intelligent, automated, and always-on, and it starts here.