CRE lending buries every deal in property financials, rent rolls, and title work across disconnected systems and teams. Underwriters re-key by hand and breaches surface in reviews, not real time, so you lose deals to faster competitors and margin to manual work.

Spent on rent roll entry and financial spreading before analysis begins

From initial borrower contact to funded loan

Covenant and reporting breaches missed between annual reviews

Deploy one agent to clear a single bottleneck, or the full suite to run CRE credit from term sheet through maturity. Each works on its own or together.

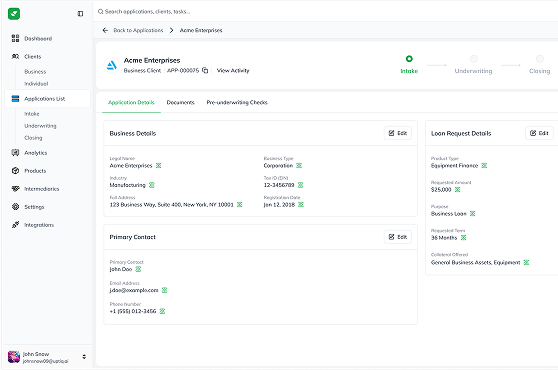

Engages CRE borrowers, pre-screens on property type, location, and LTV, and collects documents autonomously. Packages a complete application, operating statements, rent rolls, and borrower financials, before an RM touches the deal.

Reads the credit file, applies your CRE policy, and builds the risk narrative and structure. One engine for stabilized, value-add, construction, and bridge, with every ratio your policy requires.

Reads tax returns, operating statements, and personal financial statements and returns clean, structured spreads. Calculates global cash flow, DSCR, and every ratio your policy requires, with full lineage back to source.

Builds the credit memo from property analysis, spreads, risk narrative, and policy alignment. Produces a board-ready document in your format, with citations back to every source, appraisal, rent roll, and environmental summary.

Tracks every CRE relationship after booking. Monitors reporting deadlines, covenant compliance, rent roll updates, and market risk signals at the property and portfolio level. Surfaces issues before they become losses.

Every agent reads from one policy layer. Intake eligibility matches underwriting standards, which match the covenants tracked in monitoring. One policy, stabilized multifamily or value-add retail alike.

Data captured at intake flows to underwriting, then monitoring. Borrowers submit the rent roll once. Appraisal and environmental findings reach the memo automatically.

Every decision is logged with rationale, source, and policy reference. When examiners ask why a deal cleared at a given LTV or a covenant was waived, the answer is one click away.

One suite handles multifamily, retail, office, industrial, mixed-use, construction, and land. Configure once for your policy and LOS. Reconfigure when policy changes, no rebuilds.

Measurable impact from lenders across industries running the CRE Lending suite in production.

End-to-end AI agents for C&I, equipment finance, and working capital — from business intake through portfolio monitoring.

Automate SBA 7(a) and 504 workflows, eligibility checks, and form completion end-to-end.

Fast, policy-aware decisioning for small business credit at scale.

AI agents for auto, personal, and unsecured consumer credit decisioning.

Handles origination, collateral assessment, covenant tracking, and portfolio surveillance, purpose-built for the asset-based nature of the product.

Accelerate application reviews, income verification, and loan decisioning with AI-powered automation.

Pre-trained, finserv-specific capabilities the agents in this CRE suite compose on demand.

100+ pre-built integrations across cores, LOS, document systems, data providers, and CRM. Coordinate with legal before publishing the logo list.

Start with one agent or deploy the full suite. Either way, our team handles scoping, configuration, and go-live. Most banks running a single agent live in five business days. Most multi-agent deployments are in production within 30 days.