Borrowers compare your application against every digital product they use daily. When it feels slow or manual, they don't complain, they apply somewhere else. The institutions growing their consumer book are the ones that remove friction.

Spent on invoice entry, collateral lookup, and financial spreading before decisioning begins

From application submission to funded equipment loan or lease — vs. same-day decisioning from captive lenders

Borrowers choose faster competitors when lenders can't deliver decisions within hours

Purpose-built agents, each solving a specific consumer lending problem, each built to work together. Start where the friction is greatest, or deploy the full suite to transform the borrower journey.

Engages borrowers across every channel, runs real-time policy screening, and autonomously collects everything needed for underwriting. By the time a loan officer sees the file, it is ready to review.

Captures identity and KYC documentation, applying it to both the loan and the deposit, and creating a more complete banking relationship from the very start.

Replace manual statement review with one intelligent loop. From extracting raw transactions to computing complex debt service ratios, it produces decision-ready financial insights.

Every agent draws from one policy layer, so the eligibility criteria at intake stay identical to the underwriting standards in credit memos and the thresholds monitored after funding.

Every document submitted at intake flows forward automatically, to underwriting, to the memo, to monitoring. No duplicate requests, no re-entry, no starting over.

Every action is logged with its reasoning, the policy it applied, and the source it relied on. Examination-ready documentation is produced automatically.

Configured to your setup at deployment. When your policy changes or new products launch, the agents update without a technical rebuild.

Community banks and credit unions running the lending agents see consistent, compounding improvements in throughput, accuracy, and borrower experience, starting from the first week in production.

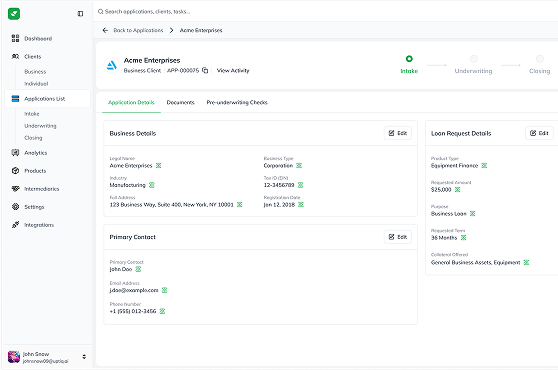

Uptiq unifies commercial loan intake, underwriting, and monitoring into a single automated workflow, enabling a focus on client relationships and risk management.

Uptiq's CRE suite is purpose-built to handle complex real estate underwriting, rent rolls, and collateral monitoring from origination.

End-to-end automation of SBA 7(a) and 504 workflows, covering eligibility and compliance so your team focuses on borrowers.

Handles origination, collateral assessment, covenant tracking, and portfolio surveillance, purpose-built for the asset-based nature of the product.

Turn customer activity into actionable insights that drive engagement, retention, and growth.

Automate SBA 7(a) and 504 workflows, eligibility checks, and form completion end-to-end.

Modular, pre-trained AI built for consumer lending data, compliance, and logic.

: 100+ pre-built integrations across cores, LOS, document systems, data providers, and CRM. Your team works in the tools they know. Uptiq handles everything running underneath.

Whether you start with one agent or deploy the full suite, our team handles every step, scoping, policy configuration, integration, and go-live. Single-agent deployments are typically live in five business days. Full suite deployments are in production within 30 days. No system replacement. No operational disruption.