SMB lending is a volume game: smaller loans, higher expectations, thinner margins. Yet most lenders still chase documents and rebuild cash flows by hand across fragmented systems.

Spent manually reconstructing cash flows and spreading financials

Driven by fragmented document collection and manual follow-ups

Front-office growth limited by manual back-office bottlenecks

Deploy a single agent to solve a specific operational bottleneck or connect multiple agents to create an end-to-end lending workflow.

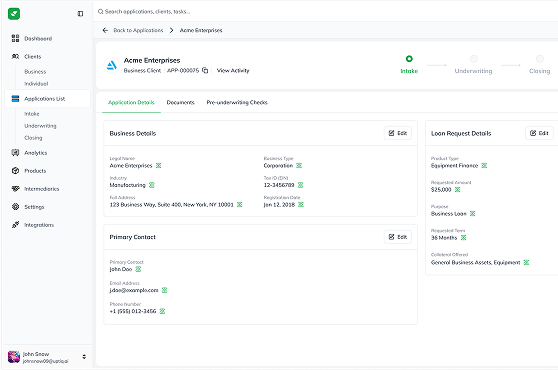

Engages borrowers across channels, collects required documents, validates application completeness, and prepares a fully packaged file before underwriting begins.

Analyzes borrower financials, applies policy rules, and generates structured scorecards and underwriting insights to accelerate credit decisions.

Automatically analyzes tax returns, financial statements, and bank data to generate standardized spreads. Calculates key credit metrics and maintains traceability back to original source documents.

Converts underwriting analysis, financial data, and risk insights into institution-ready credit memorandums. Every conclusion is supported by linked source documentatio

Continuously reviews borrower performance, covenant requirements, and reporting activity to identify potential issues before they affect portfolio quality.

Every agent works from one policy layer. Intake eligibility matches underwriting thresholds, which match the rules applied after funding. One framework, enforced from application through servicing.

Information collected once flows across the journey. Borrowers aren't asked twice, analysts aren't re-entering data, and RMs see the full borrower in one place.

Every score and exception is backed by source data, policy references, and a full activity trail. Teams explain decisions without rebuilding spreadsheets or digging through email.

Term loans, lines of credit, working capital, or SBA, the same workflow scales with volume. Add applications without adding complexity.

Measurable results from small business lenders using Uptiq's AI agents to automate SMB lending workflows.

Automate intake, underwriting, credit memo generation, and portfolio monitoring across complex C&I lending workflows.

Streamline eligibility reviews, SBA documentation, underwriting, and ongoing servicing while maintaining compliance with SBA requirements.

Accelerate property analysis, lease abstraction, financial spreading, covenant tracking, and portfolio monitoring for commercial real estate portfolios.

Automate application intake, credit analysis, document validation, and servicing workflows to improve decision speed and operational efficiency.

Pre-trained financial services capabilities that agents use across the SMB lending lifecycle.

Built with 100+ pre-built integrations across core banking platforms, loan origination systems, CRM platforms, accounting software, and open banking providers. Uptiq works within your existing environment without requiring infrastructure replacement.

Start with a single workflow or deploy a connected lending experience from intake through portfolio monitoring. Our team handles configuration, integration, and deployment, so you can begin realizing value quickly without replacing existing systems.