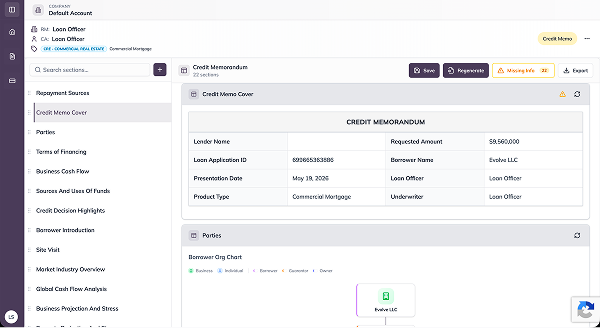

Automate bank statement analysis, business tax spreading, global cash flow assessment, and credit risk review. Deliver consistent, decision-ready credit packages without the manual work.

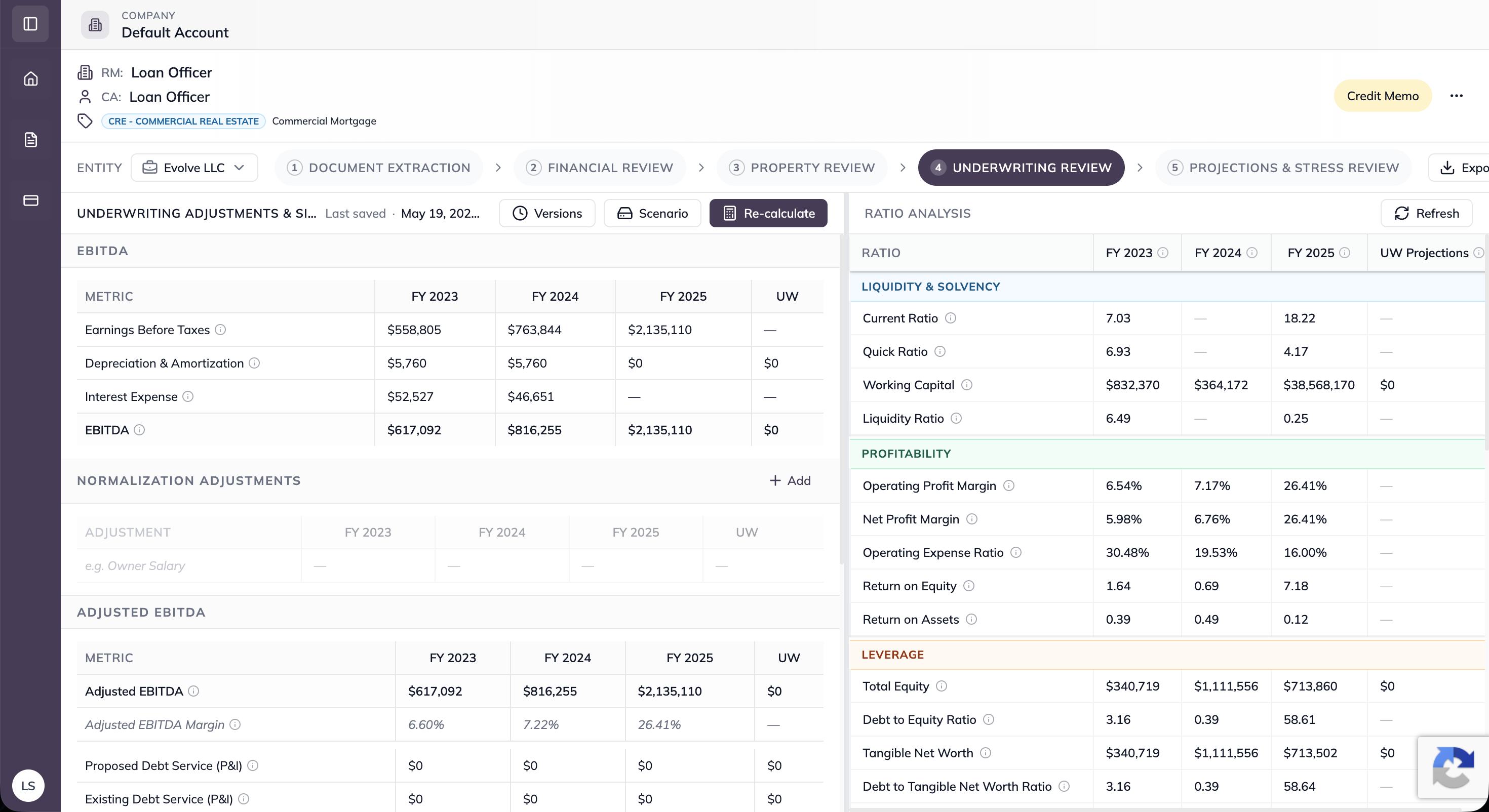

Replace manual financial analysis and credit review with a streamlined underwriting workflow that analyzes borrower financials, applies your credit policy, and delivers consistent, decision-ready recommendations in minutes.

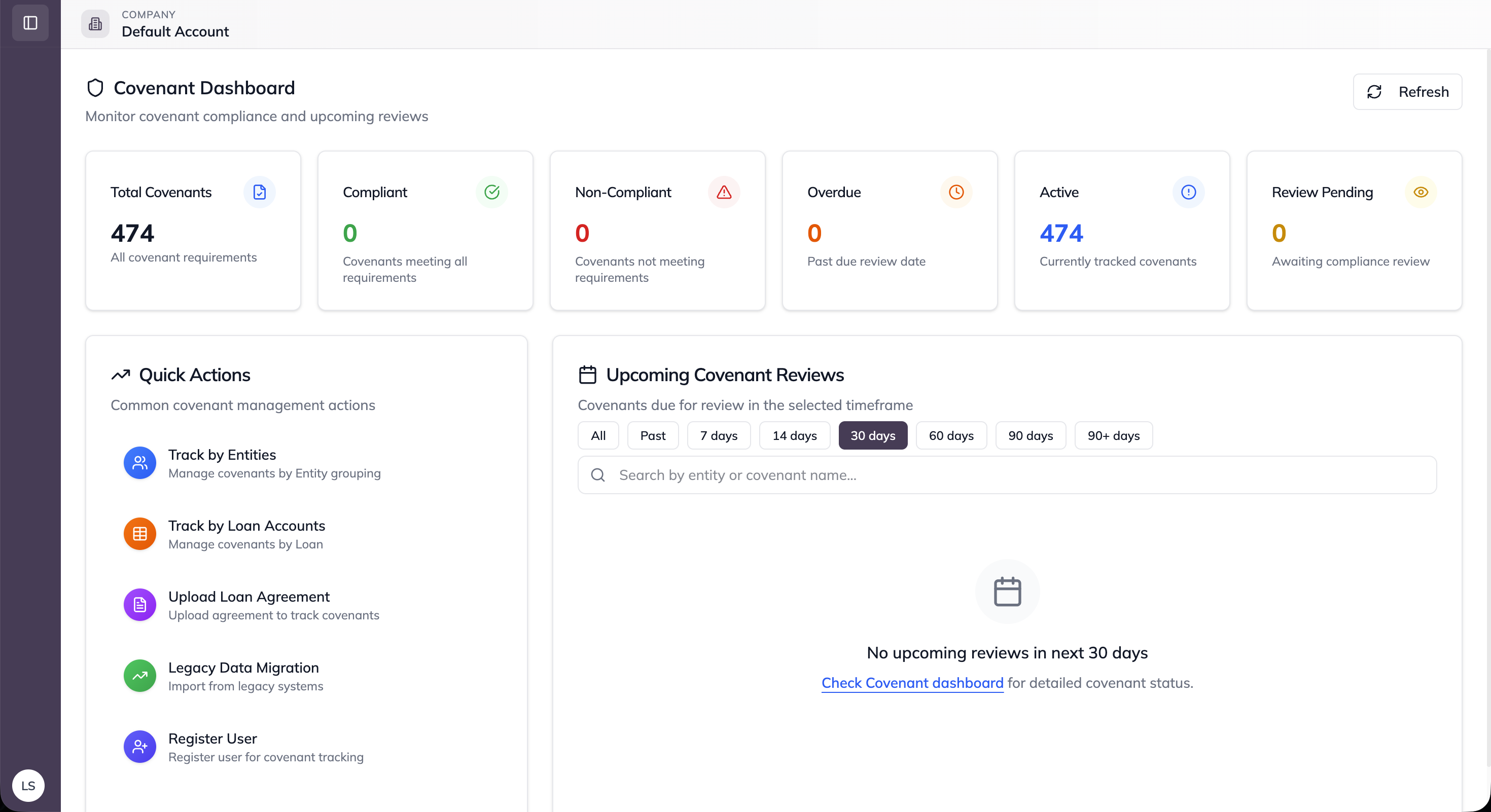

Our team handles deployment end-to-end - from credit policy configuration and bank statement analysis setup to LOS integration and go-live. Most small business lenders are in production within 5 business days, with no disruption to existing loan officer workflows.