Specialty finance, private credit, and alternative lenders run lean but the credit workflow shouldn't feel like it. Uptiq connects intake, underwriting, IC memo generation, and covenant monitoring in one AI platform, configured to your credit policy and your deal structures.

A CRM for pipeline. Excel for spreading. Word for memos. A calendar for covenants. Every handoff is a gap: deals stall, data gets re-entered, your credit team becomes the integration layer. You hired analysts to make decisions, not copy numbers between spreadsheets.

Specialty finance companies, private credit funds, marketplace lenders, and alternative lenders - purpose-built agents for the full credit lifecycle, configured to your deal types, your credit policy, and your capital partner documentation requirements

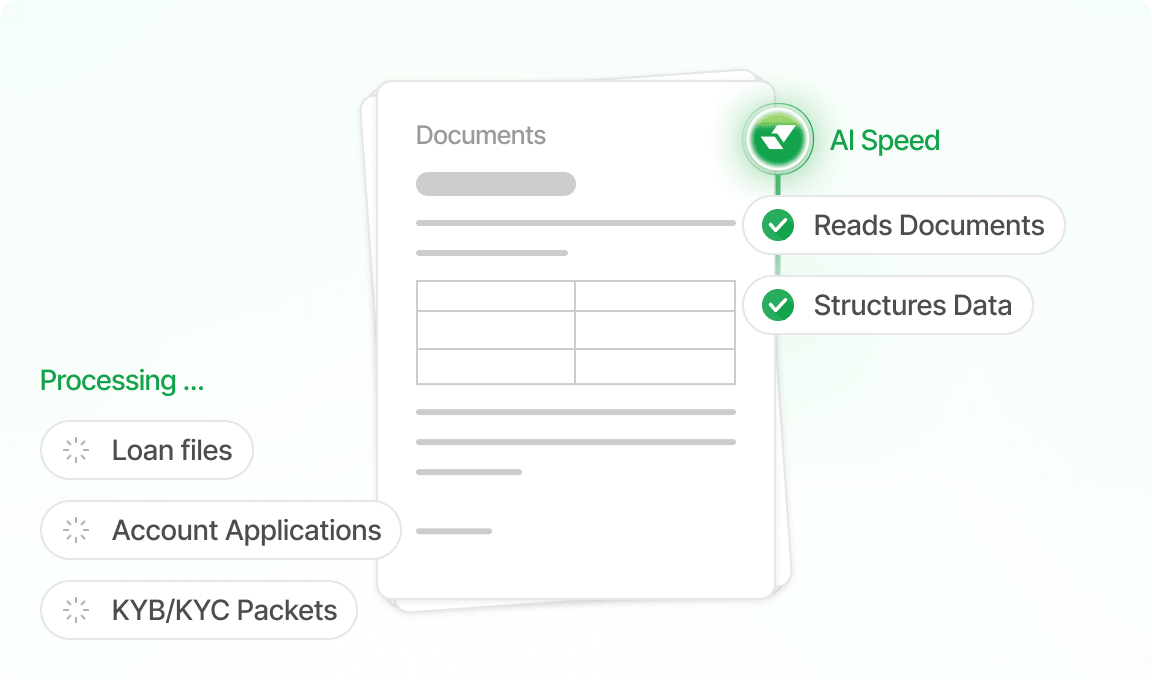

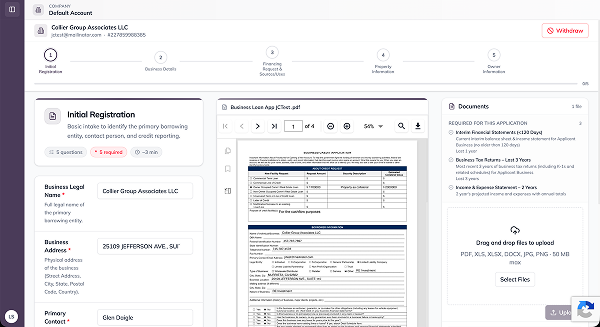

Structured borrower intake that collects, classifies, and organizes documents before they reach your underwriter - so every file arrives complete, not as a pile of attachments to sort through.

Handles multi-entity financial structures, global cash flow consolidation, guarantor analysis, and policy-mapped risk narratives - all in the format your IC already uses, without a separate spreading tool.

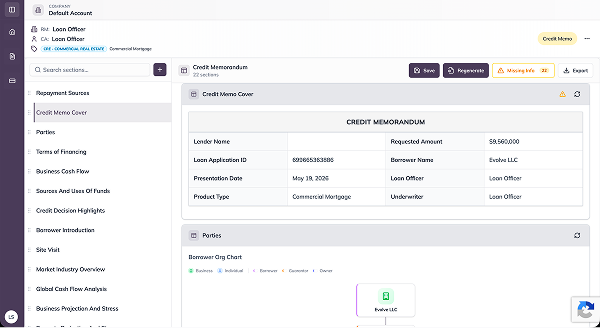

Produces a source-cited, capital-partner-defensible IC memo from the underwriting output. in your template, with every figure traceable to its source document in the time it used to take to open the Word file

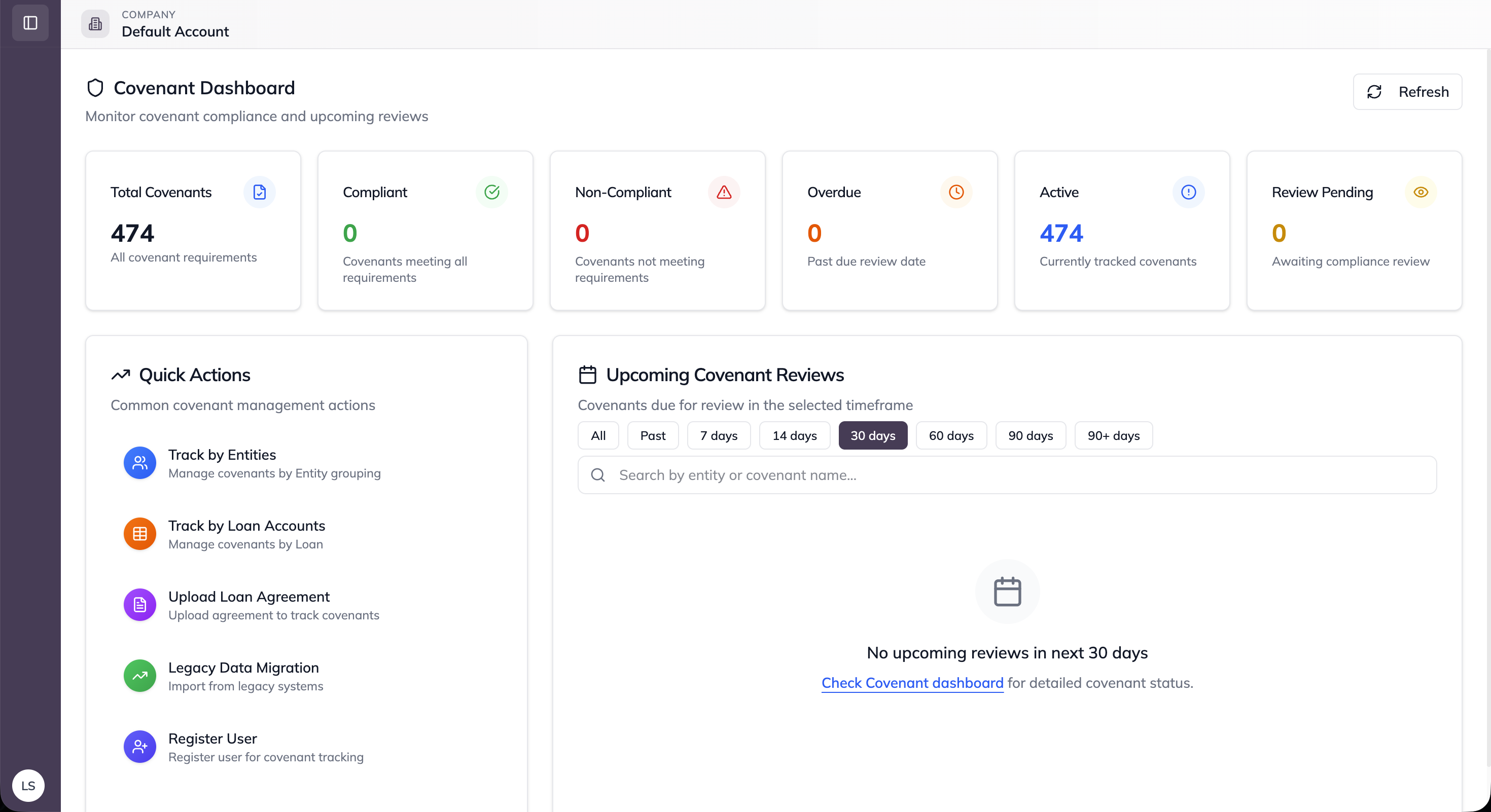

Runs continuously across your active book — covenant tests, financial reporting deadlines, borrowing base triggers, and risk flags — connected to the same borrower record built at origination. No re-entry, no reconciliation.

Measurable impact from commercial non-bank lenders running Uptiq across deal origination, underwriting, and active portfolio management.

Most non-bank lenders don't run a traditional LOS and they shouldn't have to buy one to use Uptiq. The platform connects to your CRM, your data providers, your document tools, and your portfolio management system, pushing structured credit output directly into whatever you use to run the deal pipeline.

Start with one agent in the workflow that costs your team the most time. Prove the output quality. Expand at your own pace - no renegotiation, no LOS requirement, no rip-and-replace.