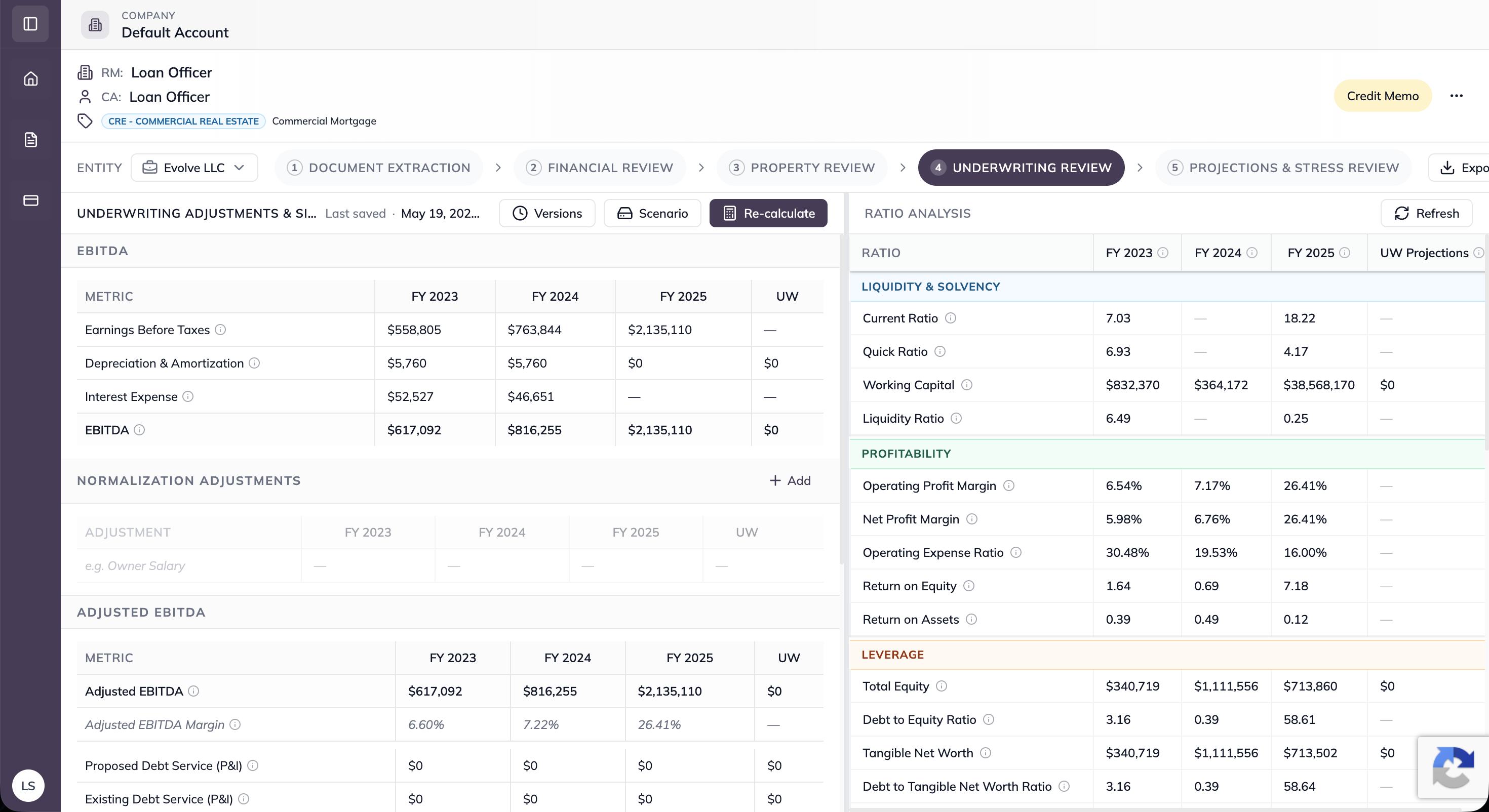

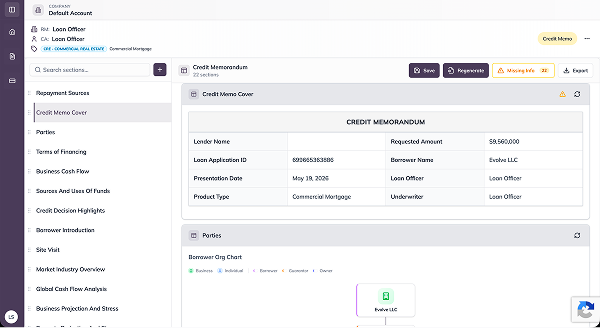

Automate rent roll extraction, operating statement analysis, DSCR modeling, and credit memo generation. Deliver approval-ready credit files in minutes instead of days.

Replace manual rent roll reviews, property cash flow analysis, and credit memo preparation with a unified underwriting workflow that evaluates property performance, applies your credit policy, and delivers decision-ready credit packages automatically.

Our team handles deployment end-to-end - from NOI model configuration and appraisal review setup to LOS integration and go-live. Most CRE lenders are in production within 15-20 business days, with no disruption to existing deal workflows.