ai innovation workshop:

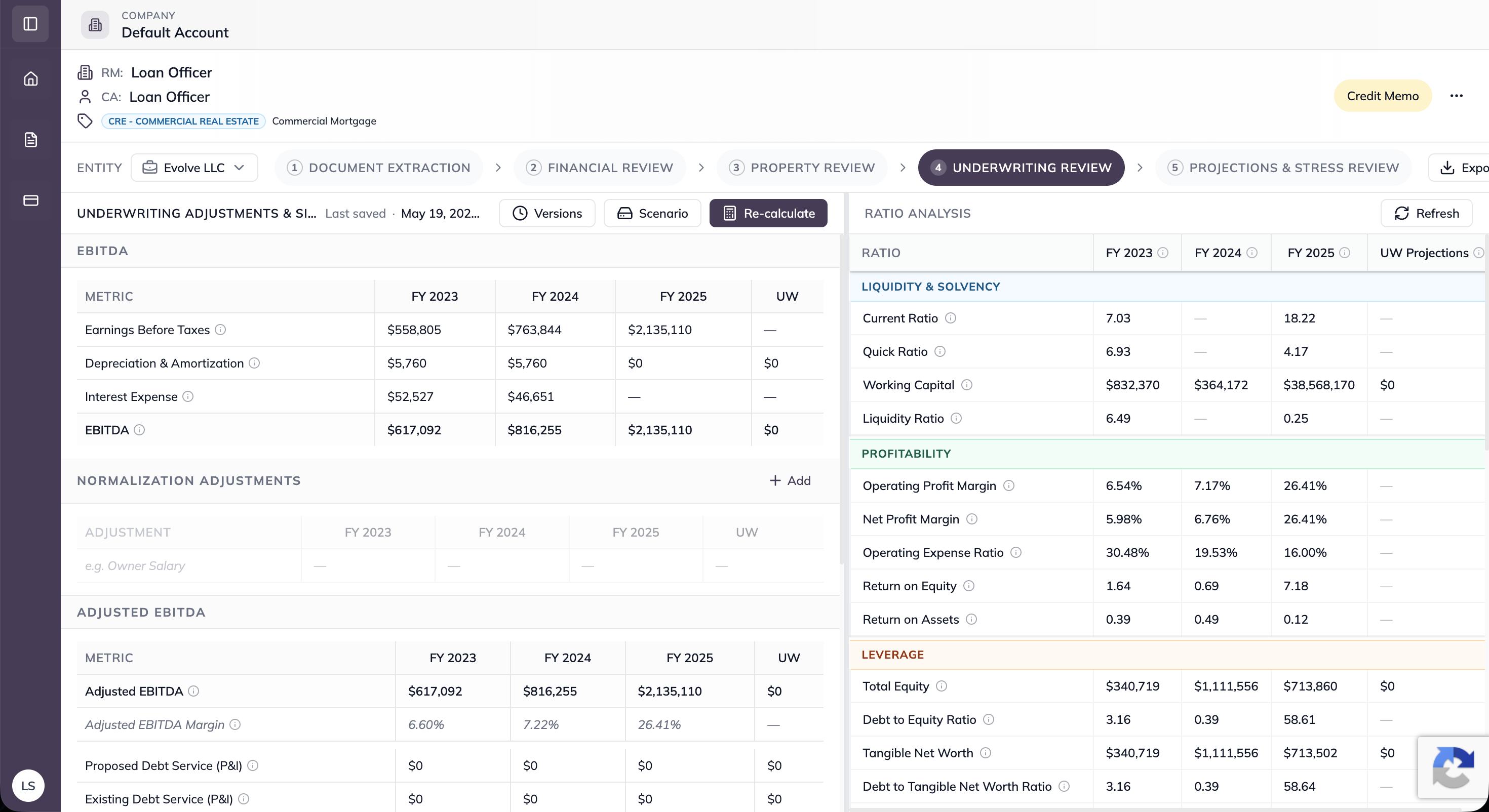

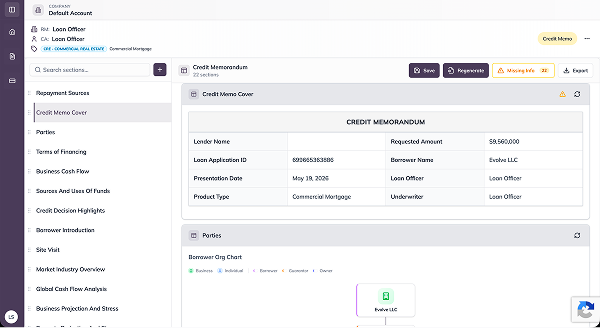

Automate deal intake, entity docs, rent roll analysis, and property financials. Every CRE application lands complete, validated, and ready for underwriting.

Automate the collection and validation of entity documents, rent rolls, property financials, and supporting information so every CRE application arrives complete and organized.

Our team handles deployment end-to-end, from configuration to go-live. Most CRE lenders live within weeks, not months.