Live Fireside Chat:

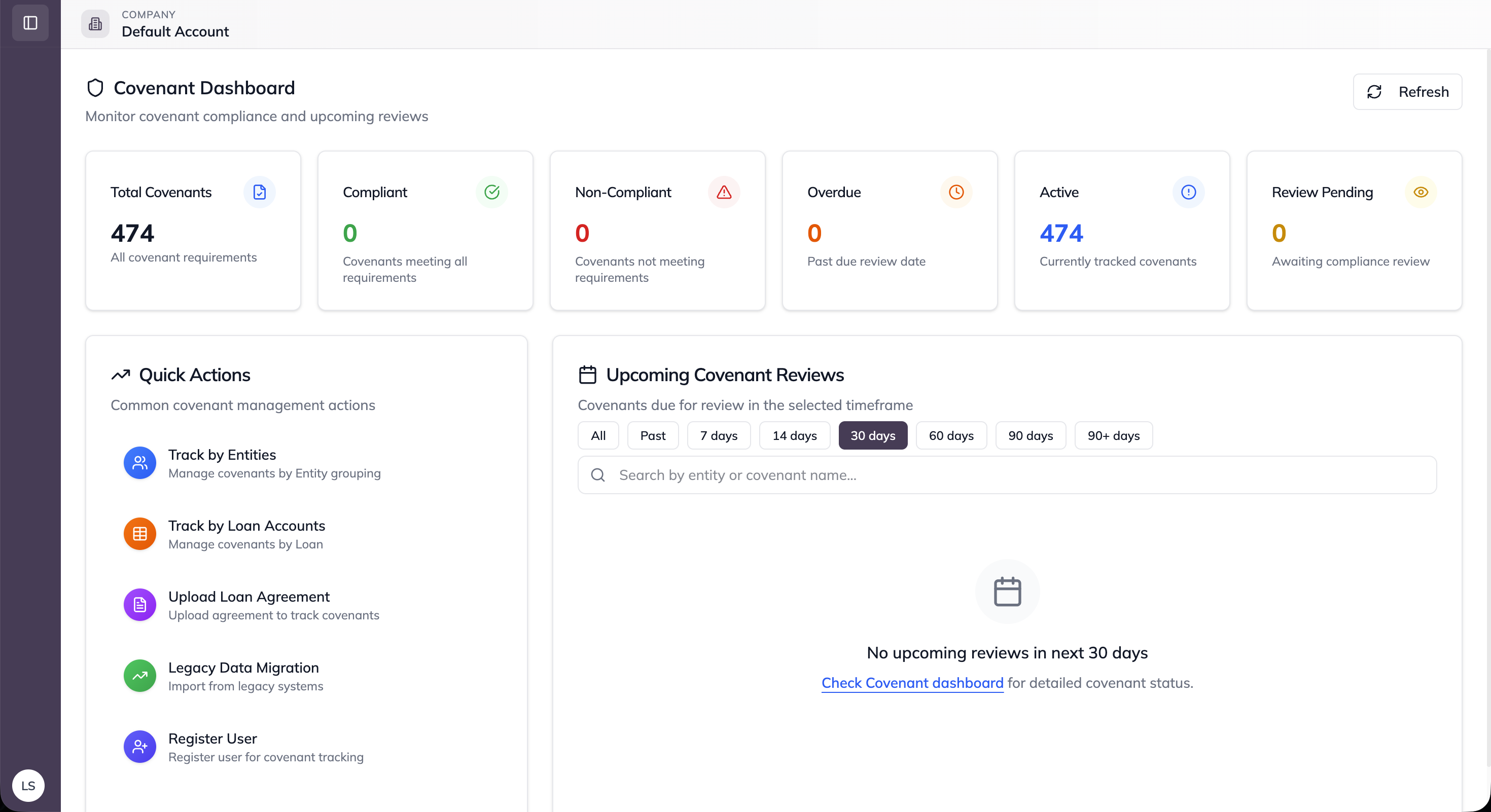

Facilitate RCSAs, monitor KRIs against risk appetite in real time, and manage operational loss events through a single integrated workflow, so the risk committee always knows where the institution stands and where it is trending.

Replace RCSA spreadsheets, manually compiled KRI dashboards, and disconnected loss event logs with an integrated risk management workflow that keeps assessments current, breaches visible, and findings tracked, without pulling risk teams away from the judgment work only they can do.

Our team handles deployment end-to-end, from configuration to go-live. Most financial institutions are live within days, and not months.