Live Fireside Chat:

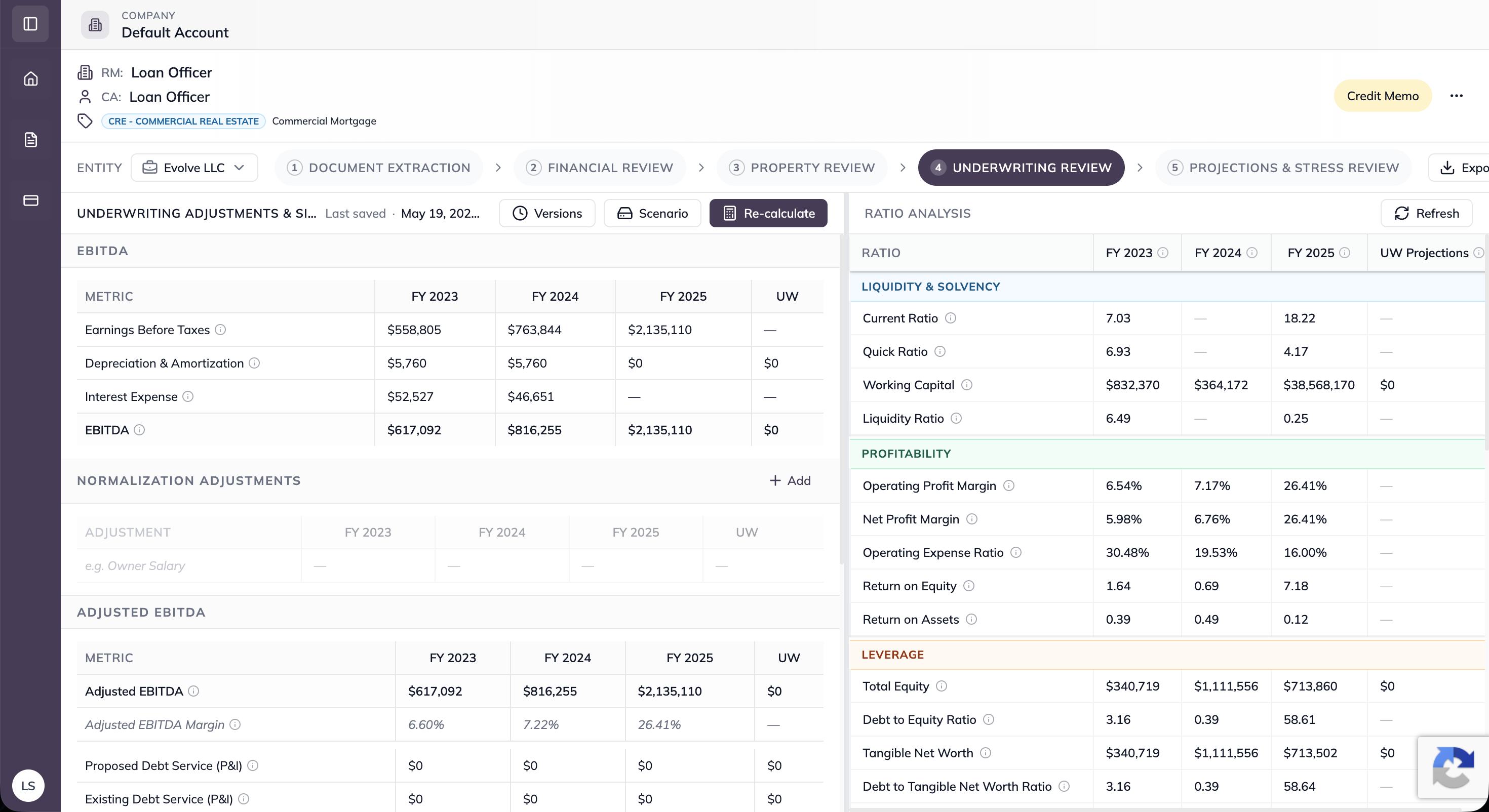

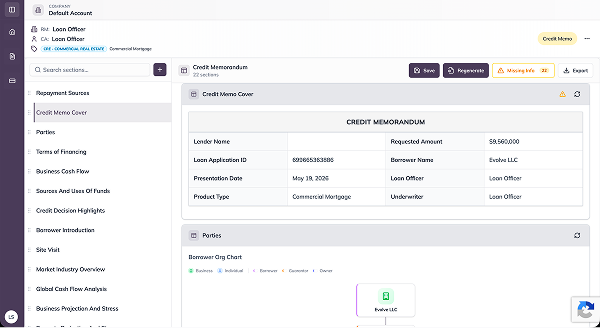

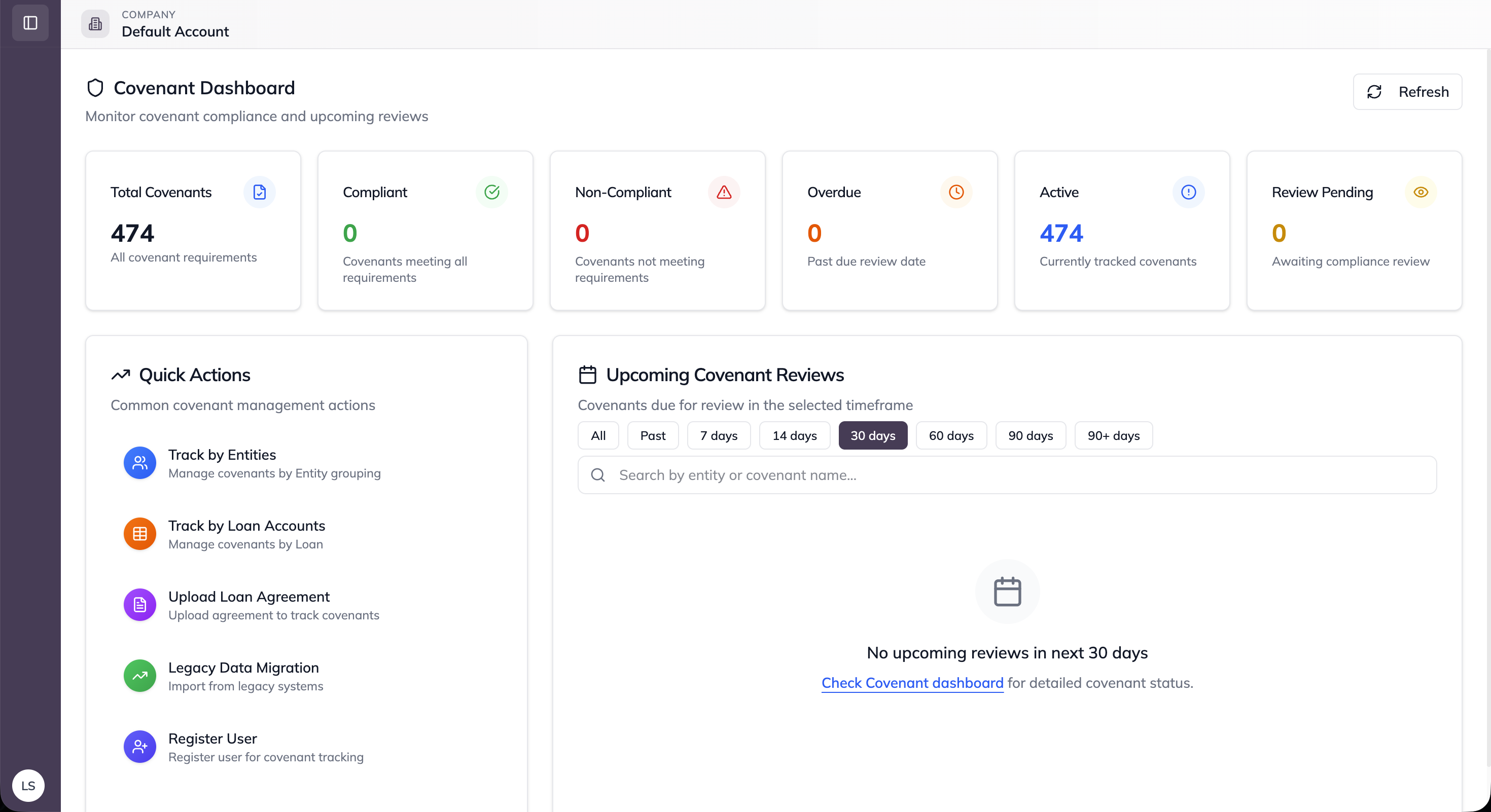

QA loan files for policy compliance, independently re-assess credit quality and risk ratings, log exceptions with defensible documentation, and track remediation to closure, while keeping origination and review completely separate at every step.

Replace sample-based file reviews, inconsistently documented exception logs, and credit rating assessments that stop at origination with a structured credit QA workflow that covers more of the portfolio, maintains clear independence, and produces the exception documentation that examiners expect.

Our team handles deployment end-to-end, from configuration to go-live. Most financial institutions are live within days, not months.