Live Fireside Chat:

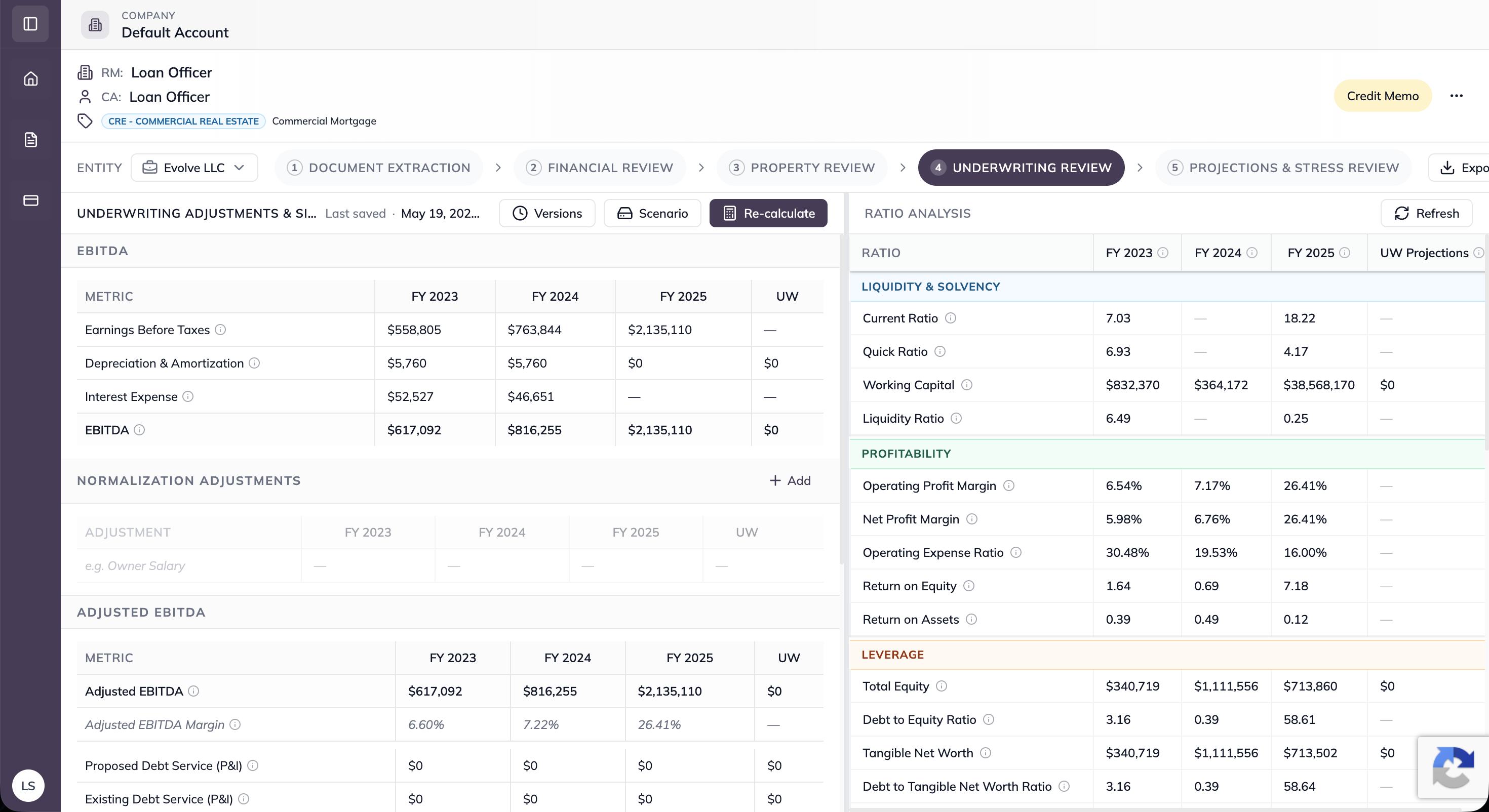

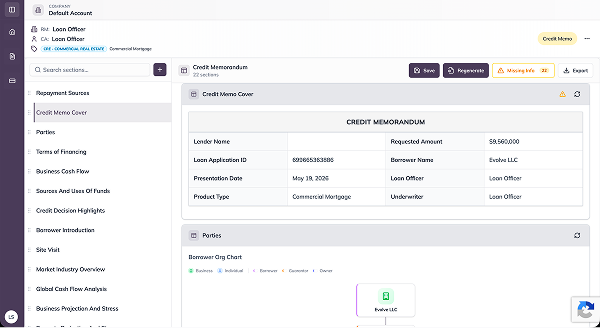

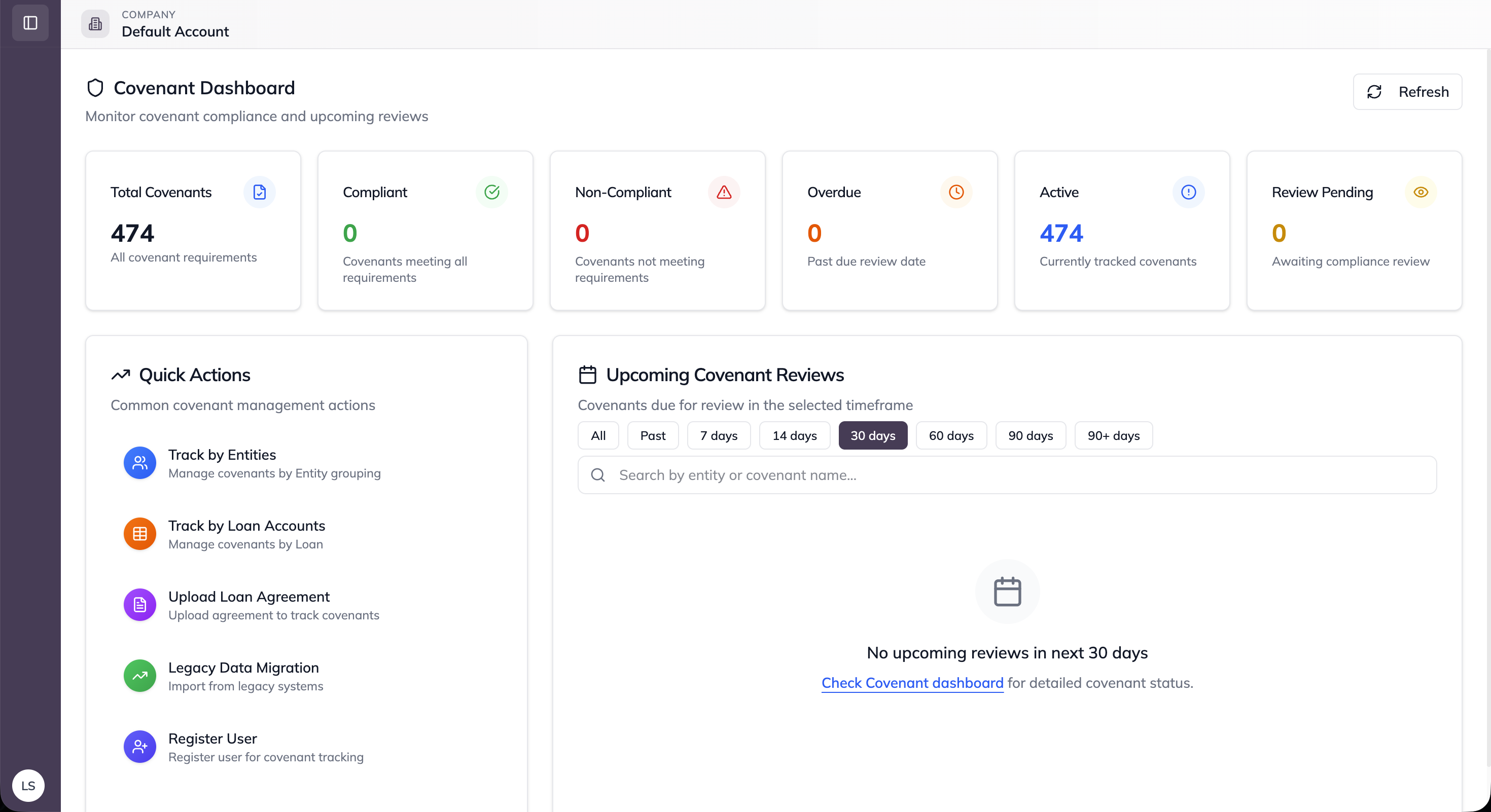

Monitor credit risk continuously across your portfolio, testing covenants, surveilling borrower financials, validating risk ratings, and supporting stress testing, so the credit committee knows where risk is trending between origination and the next annual review.

Replace annual review cycles that miss intra-period deterioration, manually assembled covenant test trackers, and stress test inputs compiled under deadline pressure with a continuous credit risk surveillance workflow that monitors every significant exposure between formal review dates.

Our team handles deployment end-to-end, from configuration to go-live. Most financial institutions are live within days, not months.